Key points:

- Agility and discernment will be essential for generating returns in an unpredictable 2026.

- Despite a strong 2025, markets enter 2026 with supportive liquidity but growing uncertainty around US rate cuts and economic momentum.

- The STANLIB Multi-Asset investment team maintains a selective risk‑on stance, recognising both AI‑driven opportunity and rising geopolitical and structural vulnerabilities.

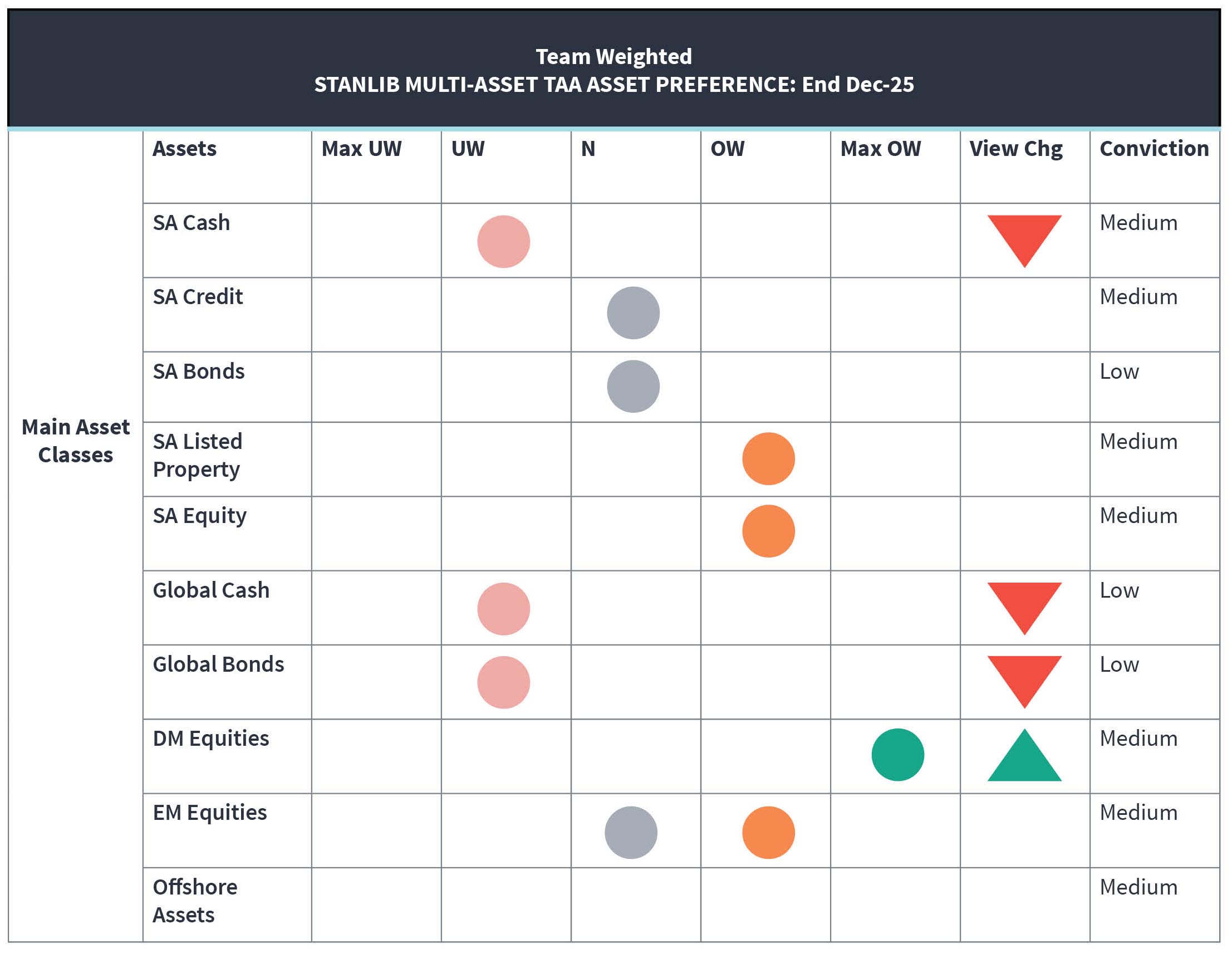

- The team’s positioning favours SA and developed‑market equities over global bonds, with targeted sector and commodity exposures applied through efficient portfolio tools.

- In 2026, diversification, flexibility and active management will be critical as policy shifts, inflation risks and global dynamics shape market outcomes.

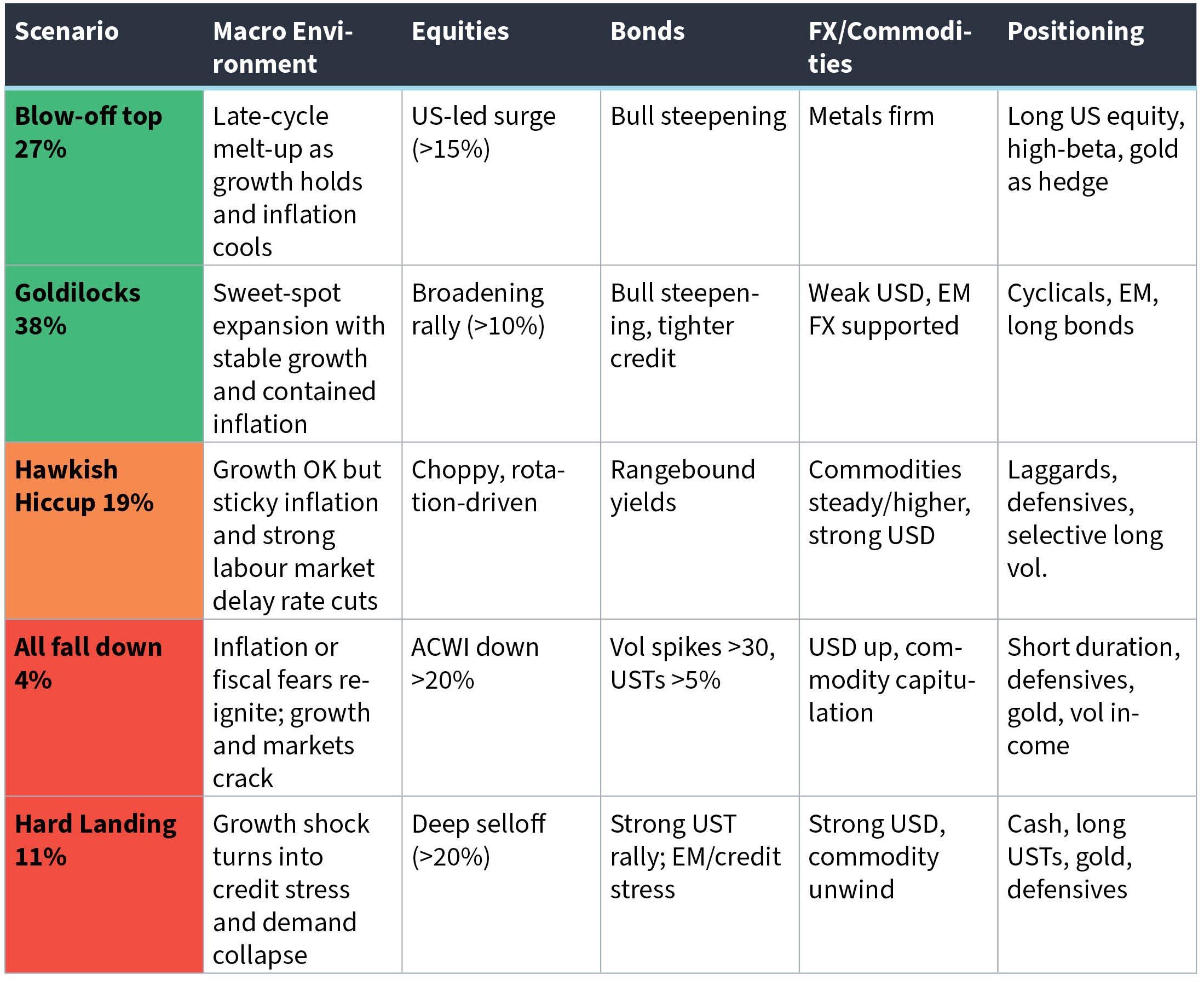

Liquidity conditions are supportive, with fiscal expansion in the US now met by fiscal support in Europe, China and, more recently, Japan. While the US rate cycle is seen as trending lower, the pace and trajectory of these cuts are more uncertain now. Our base case remains that cuts will occur, but Kevin Lings and the economics team caution that risks are growing. Kevin is worried that the exceptional vibrancy of the US economy beyond AI is waning. Fiscal risks and a change in the current downward trend in inflation are concerns and could constrain central banks’ ability to lower rates. We are already seeing this in Australia and other parts of Asia. Should the US Federal Reserve (Fed) or other central banks, find themselves caught either through rising inflation or very strong growth (or both) and given the current and growing fiscal imbalances they will be forced to hold rates stable or may even be forced to raise interest rates. Any change toward two-way interest rate risk could bring in some downside to asset markets, with bite – a scenario recently added by the team of “Hawkish Hiccup” at the expense of “New Regime” which we have carried since late in2022. In this New Regime scenario, we captured a world of rate cuts occurring, irrespective of inflation, which would support asset markets. We think this is largely played out, although a weakening job market will see more rate cuts, despite rising inflation. Given we think the market is well covered for cuts we decided to cut this scenario from our thinking.

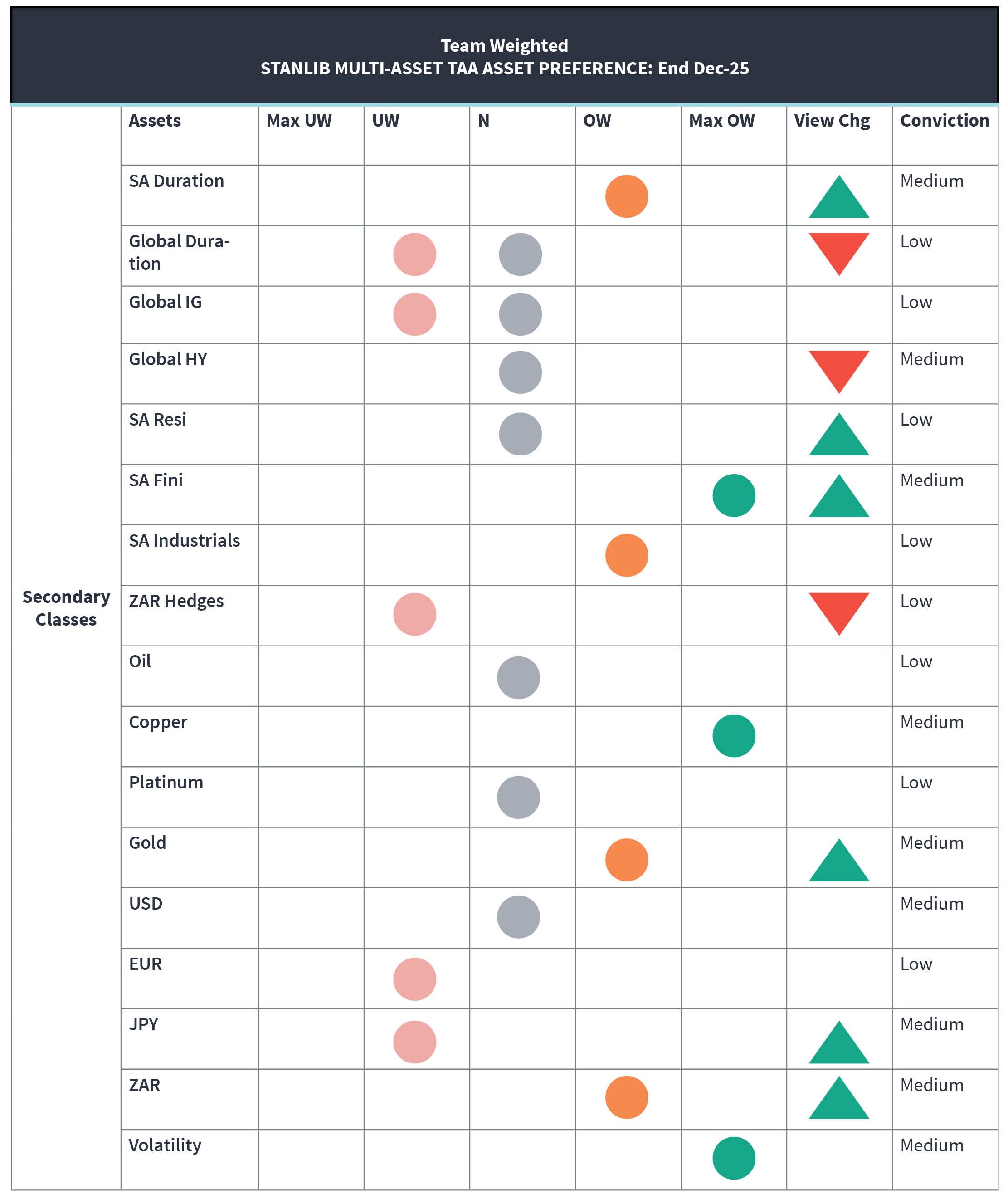

Our risk appetite is bullish but is tempered by an awareness of structural and cyclical vulnerabilities. The transformative impact of artificial intelligence for the world, its potential impact on margins and efficiencies, the ensuing capital expenditure cycle and reform-driven opportunities in markets like SA, South Korea and Japan (among others) are front of mind. Conversely, geopolitical tensions, which appear to escalate each week and signal a continuous breakdown of traditional strategic alignments, reinforce the need for genuine diversification, which is difficult to find. As a result, portfolio flexibility and nimbleness, alongside explicit hedges when tactically appropriate, underline the importance of active management in 2026. The team advocates for overweight positions in developed and South African equities and underweighting global bonds. While we like gold and other selective commodity exposures, we are mindful of inherited gold risk from our passive strategies and derivative positions, so we do not explicitly hold gold in the portfolios as an additional alpha lever, where previously we have held gold in portfolios.

In our probable scenario approach, the team’s bearish outlooks have increased, but a new “Hawkish Hiccup” scenario has emerged and was briefly outlined earlier Kevin Lings agrees with our scenario and warns that a less dovish Fed, especially as Jerome Powell’s tenure ends in May, could trigger market friction and downside risks. He says it is fair to assume that anew Fed chair will feel political pressure from President Trump and Treasury Secretary Bessent to cut rates, further and faster than data suggests. However, that raises the risk of more fiscal imbalances, credibility issues and potentially stoking cyclical and more persistent inflation, ultimately will leading to interest rate hikes, a steeper bond curve that could amplify volatility and trigger asset selloffs and currency adjustments.

As highlighted, inflation remains a pivotal factor, influencing interest rate pathways in various regions. The global rate cycle is now asynchronous, with Japan diverging from the broader trend of easing. In SA, restrictive rates and credible inflation targeting support the rand, though business and consumer confidence face challenges. Our team is constructive on growth but less so in the US than consensus. Kevin’s view is that consensus forecasts that US growth will rise to a real rate of 2%overstates the growth environment, even though the One Big Beautiful Bill will drive M&A and capex. The economics team highlights patchy soft data and delayed visibility due to government shutdowns. The economic trajectory is heavily influenced by fiscal and trade policy, immigration flows, AI capex, and geopolitical developments, making the job of the economics team even more difficult than normal. Our team has six tactical lenses, some of which show early cycle signals developing. While Kevin’s warnings are stark, he agrees that they are not yet front and centre on our tactical timeframe.

Policy developments in the US—including mid-term impacts and leadership changes at the Fed—are likely to shape market sentiment. The Fed’s focus on employment over inflation, combined with fiscal stimulus, could alter the narrative and introduce new risks for bonds and equities. The economics team is closely watching the potential appointment of Kevin Hassett as the new Fed chair, which could be a key factor in understanding US policy in2026, and how the various Fed governors behave under a new chair, as Fed independence will be fiercely protected. Mid-terms, as mentioned, will be important. Growing discourse around the K-shaped economy will probably encourage Trump to act to support lower income consumers. As his popularity and that of the MAGA Republicans wanes, expect more frantic behaviour and promises. At what point this will matter to bonds remains to be seen.

South African bonds have rallied, but further gains may be limited in the short run. The South African Reserve Bank (SARB) is expected to cut rates cautiously, with curve trades favoured over increasing our bond allocations. Credit is now tight and we struggle to see an additional credit rating upgrade in 2026. Rate cuts will be limited as inflation continues to be anchored at 3%. This makes South African bonds preferable to cash and global sovereigns, though their short-term appeal has diminished. We think that that duration, carry, and roll-down will be more important drivers of fixed income returns. This view is endorsed by our fixed income team, although they will be looking for more evidence of fiscal consolidation in the February National Budget.

Global liquidity is a major tailwind, with positive signals coming from our models in emerging markets, including SA. Central bank actions are critical, and recent developments in US curve control and “quantitative easing” signal short-term positives for equities, but they raise concerns about inflation and bond market stability looking forward but will be a powerful tailwind for equities should the belief that stealth QE is taking place (we believe it is).

Key themes for 2026 include the “early cycle” dynamic, the structural impact of AI, and the importance of diversification and flexibility. The job market in the US will be key, and we think 2026 will start showing AI impacting profits and jobs. How much it will impact consumption in the US is a key theme to watch, as we could potentially see the K-Shaped phenomenon of the US economy start to be felt by the middle class.

Emerging markets are positioned as growth engines, with attractive valuations and robust fundamentals, though selectivity is essential. South African equities and bonds offer relative value, while global equities—especially US small- and mid-caps—are undervalued compared with large caps. AI is expected to drive earnings and growth and, if our early cycle signals and thesis are correct, we want to skew away from the Magnificent 7 (or is it 10?) and broaden our exposures even more than we have already.

Gold remains a neutral asset in our portfolios. We like the asset but don’t like the position in our portfolios as an outright alpha driver, given its concentration risk in South African markets. Sector opportunities exist in South African banks and insurers, while listed property is attractive but liquidity is constrained. China’s outlook is stable but cautious, with policy support unlikely to shift consumer behaviour significantly. Currency views favour a weaker dollar, supporting emerging market currencies and the rand. We remain constructive on the rand against a variety of currency crosses.

Current Working Scenario Summaries

Multi-Asset Team Current Asset Preferences:

2026 will be seen as a year when adaptability and discernment will be the hallmarks of successful investing. The environment is dynamic, shaped by shifting policies, evolving risks, and transformative technologies. For us, the challenge is to embrace change with agility and conviction when we have it. We believe that as we remain open to new opportunities, vigilant to emerging risks, and committed to active management,2026 will present us with plenty of opportunities to deliver returns.