We started 2026 with a positive, constructive view of the market backdrop:

Our base case at the time was straightforward: Fiscal support and falling interest rates globally would underpin asset prices despite somewhat elevated equity valuations. We expected the growth cycle – supported by large capex – to be led by steady, demand-driven AI investment.

In South Africa, we expected a continued purple patch in asset prices (though likely not to the same extent as 2025). Lower interest rates, supportive global flows, commodity demand, and an improving domestic confidence backdrop were all expected to support growth and earnings. Falling bond yields would also help consumers and investment, and support physical assets (such as property).

Additionally, despite a long bull market, the environment was also showing some early-cycle behaviour, and we highlighted some points in our end-December report back slides to institutional clients:

- EU and broad US margins peaked in mid-2022 and troughed in April 2025. EM margins troughed in mid-2024. Japan is a cyclical but also a structural story now, with change afoot.

- All major global regions are therefore in the early stages of profit-margin recovery.

- We have also seen a mini-cycle in corporate high-yield defaults (notably China), likely behind us.

- Global manufacturing PMIs fell below 50 in Q3 2022. Many are still below 50, but fewer are negative, and the tone has improved. Services have had a tough three years in the base case.

- Depending on the measure, US consumer and CEO confidence is at, or worse than, COVID lows.

- Construction spend is already at a cyclical low.

- The “recovery” has both monetary and fiscal support.

- There are early signs of labour-market weakness. This is a lagging indicator, and we expect the labour picture to soften further without necessarily leading to recession –it’s partly a function of the emerging AI world. Economists may panic; we won’t.

- Inflation fears from tariff impact have not materialised, leaving room for policymakers to let the recovery run, especially as AI drives productivity gains and becomes a deflationary force in time (our base expectation).

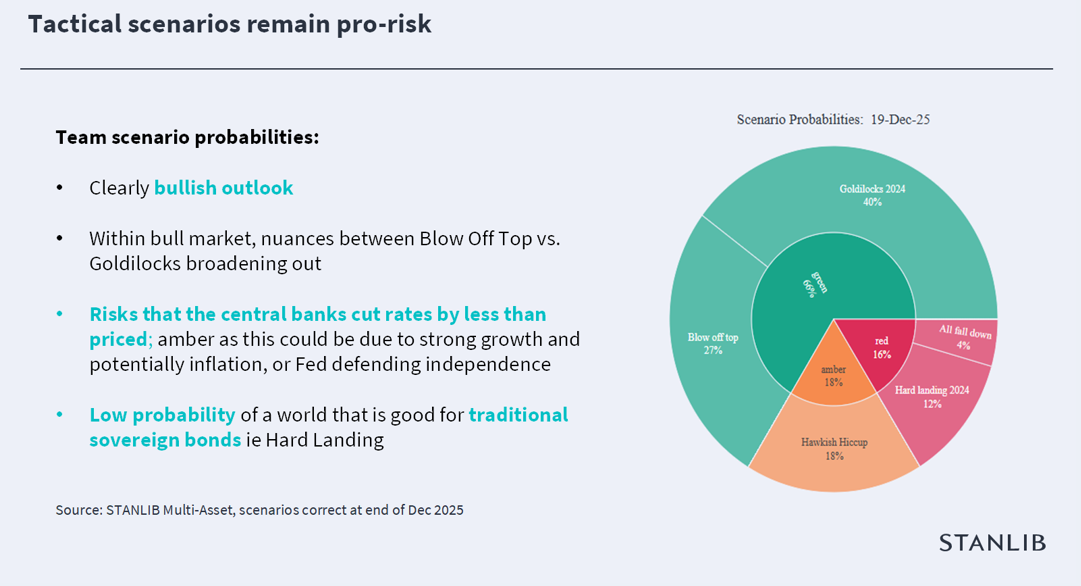

In short: Despite the risk above, our framework still pointed to a Goldilocks environment – own bonds, own equities, and keep offshore exposure limited, including limited exposure to offshore sovereign bonds (where returns are largely “risk-free”).

We did not assign a high probability to a recessionary outcome. Our All Fall Down scenario remained low probability, centred on rising bond yields and, ultimately, a slide into a fiscal bust.

Key risk: Input-cost pressure could either delay margin recovery or feed through into inflation if companies pass costs on, and hence our Hawkish Hiccup scenario was developed. This was the one that concerned us, given positioning and a fairly consensus narrative, that we broadly shared (Goldilocks scenario). We also felt that any repricing of yields higher could have an outsized impact on markets (local and global), led by bond yields. Yields could back up for several reasons – inflation, stronger growth, or fiscal concerns. The shift and shape of the curve would matter too, and we were watching closely for evidence.

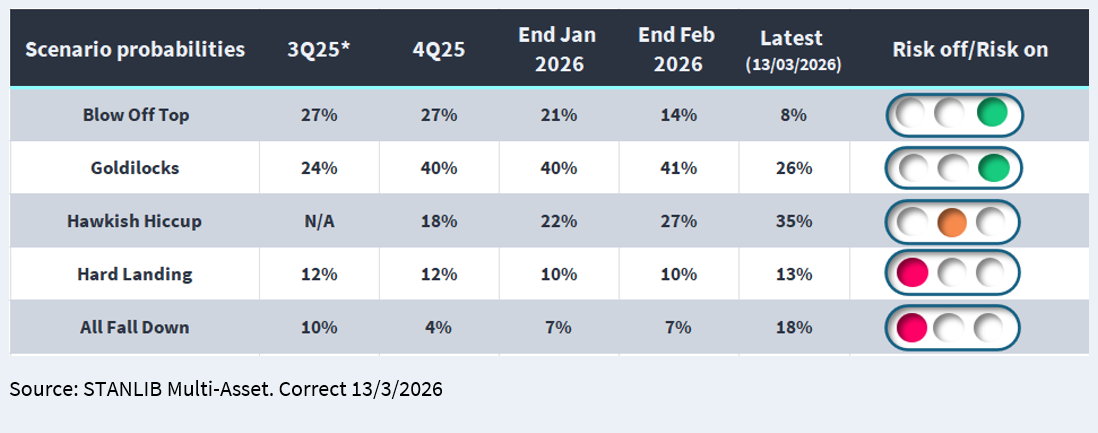

From our recent roadshow and webinar, you’ll have seen how our thinking on the Hawkish Hiccup scenario evolved, and why we started to reduce risk in portfolios in early February.

At the end of February, we wrote in our monthly commentary:

- "Policy ambition endures, but implementation faces real institutional friction.” We had seen Fed resilience, European and broader global pushback on Greenland, and a Supreme Court ruling against US President Donald Trump’s emergency powers to impose tariffs.

Later in the commentary:

- “Geopolitical risks have escalated. Tensions with Iran, long simmering, boiled over into coordinated strikes at the end of the month. Their full market impact would likely show up in March, but oil markets were already pricing in uncertainty. Brent crude rose 2.5% over the month and embedded a modest but noticeable risk premium. The key question for investors has shifted from whether geopolitical risk exists to how durably it will feed into energy costs and inflation expectations.”

In our outlook section of the monthly commentary, we highlighted (extracts):

- “Our tactical positioning remains tilted toward risk assets, although conviction has moderated from late-January levels. Within our constructive scenarios, we prefer a broad Goldilocks backdrop over a narrow, technology-driven blow-off. This distinction matters: it keeps us positive on equities overall, while recognising that leadership is broadening across sectors and regions, as we anticipated.”

- “For mandates with flexibility, we therefore prefer global equities over purely local ones, as the strongest phase of the precious-metals cycle that supported the local bourse appears to be behind us… We remain constructive on local assets and expect real returns to remain attractive, even from elevated levels.”

- “Volatility will recur, driven by geopolitics, evolving AI dynamics, and pockets of stress in private credit. However, given the still-constructive global and domestic backdrop, we expect periods of weakness to create selective buying opportunities. We are positively positioned and willing to take risk – but hyper-alert and flexible.”

In late February, our Goldilocks view – and the potential for an unusually strong return profile – was further supported by bull flattening in global bond curves, from Japan to Europe to the US, including South Africa. We had expected this first in Japan (we have said QE, or yield curve control, is in play in Japan and to lesser degrees in a few other countries). Our work showed strong returns from a variety of assets within that “regime”.

Despite the work, pointing to owning risk assets and especially gold in the Goldilocks and bull flattening world, we reduced SA equity risk on concerns around the gold move – higher gold and higher volatility, an unusual combination. Additionally, concentration risk in SA equities (more than 30% in precious metals) was/is incredibly high. At the same time, our correlation signals suggested SA equities, SA bonds, and USD/ZAR were 0.85, 0.75 and 0.55 correlated to gold. In practice, diversification benefits were limited, so we reduced risk relative to our Goldilocks base case.

- We felt the bigger risks sat in gold and the rand. As a result, the risk reduction was mainly implemented through SA equities at an index level, while keeping some exposure to SA financials, property, etc. We also increased offshore exposure in our Regulation 28 fund slowering SA exposure, as we still wanted to run our fixed income view.

- We also reduced exposure to global high-yield credit (a small allocation) on 3 March. We’ve been tracking private credit and private equity for years and have written extensively on the topic. Stress in private credit has spilled into leveraged loan markets and we expect high yield corporates to begin to feel the impact of spread widening. We felt it was only a matter of time before this started to impact listed credit markets as well.

Where we are now:

Events in the Middle East have escalated and we’re now two weeks into what Trump referred to as a short-term “excursion”. Markets – and we were no exception – were initially somewhat complacent. History often suggests buying the early sell-off in risk assets at the start of a war. But the Strait of Hormuz is a critical bottleneck for oil, gas, and refined products, with a meaningful share destined for Asian markets, although not exclusively. Until last weekend, the Hormuz threat still felt relatively contained.

In our view, escalation stepped up since last weekend (7 March) with targeted Iranian strikes into Gulf Cooperation Council (GCC) states. The elevation of Ayatollah Khamenei’s son, Mojtaba Khamenei, to Supreme Leader entrenches the regime further. Israel’s attack on Iranian oil infrastructure, along with targeted attacks on Islamic Revolutionary Guards in Beirut, increased the probability of a broader regional escalation, and reduced the likelihood of a quickly negotiated end to the “excursion”.

During the past few days, the Strait of Hormuz is in play: Ships have been sunk, mines are being laid by Iran, and the route has been effectively blocked, with almost no vessels moving through the strait. Iran still has cards to play, despite Trump thinking the opposite.

Oil prices have risen, lifting inflation expectations, and oil prices are now rising along the oil curve, signifying a growing realisation that the quick exit possibility is diminishing quickly. Rising inflation expectations are pushing expected rate cuts further out across many markets. Remember, we and others have been positioned for a rate-cutting environment. Markets are now even pricing in hikes in Europe, the U.K, and South Africa, Australia was already in hiking mode. Positioning has been caught on the wrong side, and consensus trades have been punished. South Africa is no different, and March has so far delivered on our fear of the impact of a Hawkish Hiccup

So far in March, the scoreboard is ugly:

- SA bonds: -4.99%

- SA listed property: -12.14%

- SA equities: -10.43%, physical gold -4.91%, Brent Crude +41.54%, platinum -14.38%

- ZAR: -5.88% (spot) vs USD

- Global emerging markets -8.77 ($)

- S&P 500 -3.59%, Japan equities -8.55%, European equities -6%

Trump has a habit of changing course. The Financial Times called him TACO Trump (Trump always chickens out), and we expected this time to be no different – but he isn’t the only actor. As noted, Iran has cards to play, and it is playing its good cards now.

A widening conflict and rising oil prices, alongside supply pressures yet to feed through into energy, gas, and downstream products, raise the risk of inflation (already visible in fuel prices). At the same time, they increase the risk of a growth hiccup, not just an inflation hiccup. Until the war, we certainly hadn’t ascribed a high probability of a growth slowdown (our Hard Landing scenario). Hard Landing could come, especially if there is an impact on the semiconductor supply chain. Semiconductor manufacturing relies on helium for cooling and ultra‑clean processing; fabs consume ~25% of global helium supply, around 30% is produced in Qatar and shipped via the Strait of Hormuz. A protracted supply disruption here, which is critical to the AI, capex, and commodity cycles that has been the tailwind behind the Goldilocks world we envisaged. Oil and refined product prices increasingly reflect that realisation, especially as it will take time to restart production in the region. Even if Trump were to declare victory tomorrow, significant supply interruption is upon us, as well as an ensuing impact on energy and other input materials that need to travel through the Hormuz gauntlet.

As mentioned earlier, we’ve also been watching private credit closely. Stress is building and gates have been introduced to limit withdrawals from some funds, creating shocks. In credit, you sell what you can, not necessarily what you want. We are at an early stage, but high-yield markets globally are seeing spreads widen. While some of this may be a risk premium tied to oil and rising cost pressures, credit is becoming a bigger issue.

Summary through our process lenses:

A potential regime shift/inflection point may have arrived sooner than expected. Four large factors are converging at once, and the Iran conflict adds supply and growth shocks that increase downside risk.

- The damage from inflation is already being done. Even if Trump retreats or declares victory, our confidence that markets will simply “look through it” is low. The impact of the supply disruption in oil and refined markets will place upward pressure on inflation readings. The market has already priced some of this. Should inflation prints start rising fast, the previous path of rate cuts has been interrupted and makes navigating a potential growth shock by cutting rates difficult, especially with inflation scars from the previous few years.

- Credit stress, which was in play prior to the war, has increased, and could trigger its own domino effects –even without further Iran-related disruption.

- AI’s impact on jobs is starting to show up in labour markets, adding pressure on consumers.

- We still believe AI will ultimately boost margins and productivity, but there’s a transition phase to get there.

- Central banks now have a tougher balancing act, especially if they also need to cushion weakening labour markets.

- Fiscal stress is now likely to rise further, with the cost of war reported at around $2 billion per day for the US.

- Even with higher yields, which should appeal to many investors, Germany’s bond auction “failed” on Wednesday.

- Yield curves are still behaving for now, but fiscal stress tends to surface at the long end. So far, only the UK is showing tentative signs, with the long end moving higher again.

Across our process, several lenses have deteriorated at the same time. That’s pushed the team from “is this just noise?” to protecting against asymmetric left-tail downside (even if short-term squeezes remain possible).

Economics (inflation + growth hit): Middle East escalation and higher oil prices – plus downstream/refining risks – are increasingly looking more persistent (infrastructure damage, freight/insurance, port congestion). That’s more stagflationary pressure than a clean inflation-only shock that our Hawkish Hiccup scenario was built around.

- Momentum (turning fragile): Indices are only modestly off their highs, but short-term momentum is weakening. Long-term signals remain positive – nota bear signal yet – but markets look less resilient to shocks.

- Liquidity (key deterioration): The rate of change in broad global liquidity is turning negative (notably across DM). When negative liquidity becomes extreme in breadth, equity drawdown probabilities rise sharply – so the team has moved this into “at-risk watch”.

- Volatility is not fully pricing the macro and credit risks we’re seeing.

- Sentiment screens could argue for adding risk, but we think the regime is shifting and positioning remains crowded.

- Valuations offer poor asymmetry (limited upside vs meaningful downside), which supports a bias to sell rallies, raise cash, and add protection/convexity – though that alone isn’t sufficient.

We have made adjustments to all our portfolios, but I wouldn’t say we are where we need to be should probabilities ratchet higher for our negative market outcomes. Hawkish Hiccup has happened, at pace. We have likely already seen the impact in market prices, but not yet the reaction function from central banks which affects the evolution of pathways from here, although not exclusively.

In conclusion

Across our current scenarios above, conviction is low on where we go from here. But the upside/downside payoff profile looks skewed more to a left tail than significant market upside. This has us keeping risk contained and looking to reduce opportunistically – unless we see a clear shift in direction across the four highlighted verging risks outlined above, which we think are now converging into a potential regime change for markets.