Key takeouts:

- Private‑credit stress is starting to surface in areas such as software‑linked loans and direct lending; listed business development companies (BDCs) are simply the first place where that underlying pressure is being priced daily.

- US high‑yield spreads have barely moved so far, which may be the biggest risk: while headline indices still look relatively calm, certain areas, including leveraged loans, have already started to show renewed strain since early 2026.

- Software, now one of the largest sector exposures within US private‑credit portfolios, is under pressure as AI challenges long‑assumed revenue durability, with knock‑on effects into valuations, recoveries and refinancing prospects.

- Liquidity "gates", maturity extensions and payment‑in‑kind features show that stress is being managed and deferred in private markets, not eliminated, and that investors in semi‑liquid products may face limits just when they most want to exit.

- These shifts confirm why a structured, multi‑lens investment process and forward‑looking scenarios are essential when managing listed portfolios through a turning credit and liquidity cycle.

A seven‑year journey of warning signs

Back in 2019, the first Unicorns article (Unicorns: a warning sign for modern-day markets) explored how ultra‑low interest rates and negative‑yielding government bonds were distorting investor behaviour. Capital was flowing into unlisted companies with limited transparency, often at valuations that relied more on abundant liquidity than on business fundamentals.

In 2023, the second article (Unicorns revisited: reaching new levels of irrational exuberance) revisited that theme after the pandemic‑era wave of monetary and fiscal stimulus. Central banks were finally forced to raise interest rates to combat persistent inflation, and we cautioned that business models built on free money would be tested.

By 2025, the third article, (The Private Mirage), focused on the opacity of private assets. It highlighted how smooth, low‑volatility return series are often the result of infrequent pricing, internal valuation models and delayed recognition of losses rather than genuine resilience.

Now, in early 2026, the stresses discussed over the last seven years are beginning to appear more clearly. Not in dramatic headlines or across every asset class, but in the parts of the market that usually react first when liquidity tightens.

From cheap money to private credit boom

The story of private credit cannot be separated from the broader backdrop. For most of the past decade:

- interest rates were at or near record lows

- central banks expanded their balance sheets aggressively

- investors searched for yield in every corner of the market

Banks, facing tighter regulation after the Global Financial Crisis, reduced certain types of corporate lending. Private‑credit funds and business development companies (BDCs) stepped into the gap. (BDCs are listed vehicles that loan to mid‑market companies, essentially taking a private‑credit model and listing it publicly). They offered loans to mid‑sized and leveraged businesses at attractive yields, often with floating‑rate coupons and relatively loose documentation.

For investors, this looked appealing: higher reported yields than traditional bonds, lower reported volatility than listed high yield, and the impression of diversification away from public markets. Over time, private credit grew into a large and increasingly systemically relevant financing channel, with significant exposure to sectors such as software, healthcare, business services and industrials.

The key question now is how this ecosystem behaves in a world where rates are higher, refinancing is more demanding and some business models are being challenged by new technologies.

Early stress in private credit: the listed canary

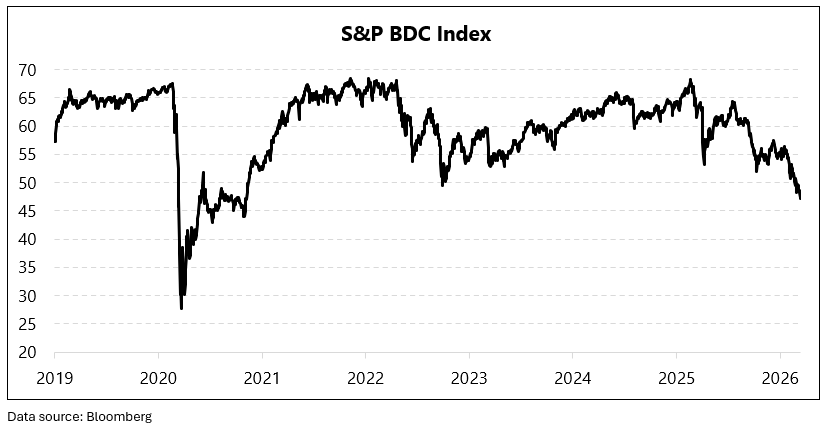

One of the clearest signs of emerging pressure is reflected in listed BDCs*. The S&P BDC Index has fallen meaningfully from its highs and has underperformed the broader equity market in recent months.

BDCs matter for two reasons:

- They hold substantial portfolios of loans to mid-market, often leveraged companies.

- Their share prices are set in real time by the market, rather than by internal valuation committees.

When BDC prices weaken while private‑credit net asset values still look stable, it is not because one set of loans is healthy and the other is not. It is because the underlying portfolios are facing growing pressure, and listed vehicles are simply forced to acknowledge that reality sooner. Listed BDCs cannot delay price discovery. However, private‑credit funds, with quarterly reporting and internal models, can.

If that gap persists, the pressure visible in BDC equity prices is likely to spread into other parts of the credit market as well, especially in more leveraged parts of the ecosystem.

What spreads and structures are telling us

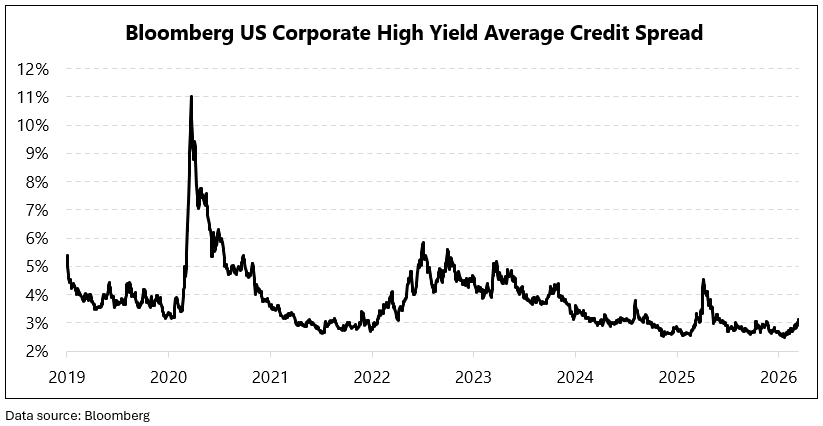

Looking at broad US high‑yield credit spreads, the picture appears more benign. Spreads remain significantly below the levels seen during the COVID shock, and there has been no dramatic blowout. That said, leveraged‑loan indices began to widen again in early 2026, even as headline high‑yield spreads remained range‑bound.

However, the apparent calm hides important nuances:

- spreads have stopped compressing and, in some areas, have drifted higher

- in specific sectors, notably software‑linked loans, spreads have moved back towards levels associated with previous stress periods

- the proportion of loans trading at distressed levels in these pockets has risen from very low bases

The tension today is that parts of private credit and the BDC universe are already showing clear signs of strain, while broad US high‑yield spreads are still relatively relaxed. That disconnect is the root of our concern. In previous cycles, publicly traded credit often adjusted later, but then moved quickly once stresses in less transparent parts of the system became harder to ignore.

In addition, some of the tools being used to manage stress are themselves signals. There has been a noticeable increase in the use of payment-in-kind (PIK) interest and maturity extensions, which conserve cash for borrowers but increase risk for lenders. Liquidity "gates" in retail-orientated and evergreen vehicles, which limit how much can be redeemed in a given period, are being activated more frequently as investors reassess their exposure.

Taken together – widening pockets of stress in private credit, more creative structures to avoid recognising losses, and an apparently calm high‑yield index – this looks less like a system that is“ reassuring on the surface” and more like one that has not yet fully priced the risks already visible in private markets.

Software, AI and a new weak link

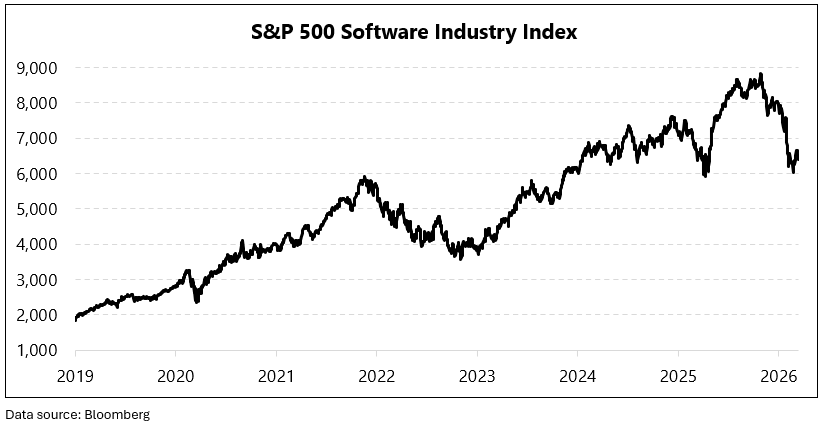

The sector composition of private credit is central to understanding today’s risks. Over the past decade, software and technology‑enabled businesses have become some of the most popular borrowers. The logic was straightforward: recurring subscription revenues, high margins and low capital intensity made them appear ideal from a lending perspective.

For this reason, software has become one of the largest single sector exposures in US private‑credit portfolios. It now accounts for roughly 20-25% of these portfolios, according to Deutsche Bank, which is a larger concentration than Telecoms held in the high yield bond market in 2000. As a result, the current pressure is not just a sector wobble; it is a portfolio level risk.

This narrative is now being challenged. The rapid emergence of agentic AI tools, which are the next generation of AI assistants, is changing how businesses automate tasks, use data and pay for software. In some cases, AI is compressing traditional pricing models or displacing products entirely. In others, it is forcing companies to invest heavily simply to remain competitive.

The consequences for credit are twofold. First, equity markets have already de‑rated many software names, as investors reassess growth and cash‑flow trajectories. Second, some software‑linked loans have moved into distressed territory, with spreads and pricing now closer to the levels seen in the COVID period than to those of the recent boom.

For private credit, this is particularly important because:

- many loans were underwritten in a world of low rates and optimistic revenue assumptions

- the use of flexible structures, such as PIK and covenant‑light documentation, can delay but not remove the recognition of stress

As with the original unicorns discussion, the lesson is that a popular sector with seemingly predictable growth can still become a weak link if too much capital chases similar ideas without enough attention to safety margins.

History suggests that stress rarely stays neatly contained in one corner. A decade ago, shale‑energy credit looked like a local issue before its effects spread more widely through credit markets. Today’s software‑linked pressures could play a similar role if lenders are exposed in similar ways across multiple portfolios.

Oil, inflation and the macro backdrop

Sector‑specific issues are emerging against a macroeconomic backdrop that is itself more uncertain. The recent spike in oil prices, driven by renewed tensions in the Middle East, has raised concerns about inflation just as markets had begun to anticipate interest‑rate cuts.

Higher oil prices affect credit through several channels, including:

- squeezing household budgets, reducing discretionary spending

- raising costs for energy‑intensive industries, pressuring margins

- making central banks more hesitant to ease policy too quickly

For leveraged borrowers facing higher interest costs and more cautious lenders, these pressures are unhelpful. If private‑market financing conditions tighten further, and if defaults and restructurings rise from very low levels, policy makers may be forced to weigh financial‑stability considerations alongside inflation in their decision‑making.

Why this matters for listed portfolios

For investors in listed portfolios, it may be tempting to see these developments as confined to private markets. In practice, the links are closer than they appear.

There are two key reasons for this:

- in the capital structure, creditors rank ahead of equity, i.e. when a business runs into trouble, equity is the first to be wiped out

- private‑credit funds, BDCs and banks all provide financing to companies that are also represented in listed equity and bond markets, directly or indirectly

If stress in private credit escalates, it can tighten financing conditions for a broader set of companies, lead to higher default expectations in public high yield, and ultimately weigh on equity valuations. This does not mean that all areas will be affected equally, but it does mean that listed portfolios cannot ignore what is happening in the private domain.

This is where a structured, through‑the‑cycle process becomes essential. The multi-asset process uses six lenses, including liquidity, valuation, economics, sentiment, volatility and momentum, to assess risk and opportunity across asset classes. While liquidity and valuation lenses have been particularly important in analysing private-market developments, the strength of the framework lies in its ability to bring together multiple perspectives rather than relying on any single indicator.

Forward‑looking market-scenario analysis forms the second part of this process. Rather than positioning for a single forecast, scenarios explore how different asset-class return combinations may unfold. In the current environment, market scenarios that consider the risk of the market pricing out the assumed further central bank rate cuts, or more persistent inflation feeding into weaker bonds at the same time as weaker equities, or slower growth that could see longer duration bonds act as protection for any equity wobbles, are especially relevant.

Conclusion: process over prediction

The current phase of the cycle is characterised less by dramatic headlines and more by subtle but important shifts in credit, liquidity and sector dynamics.

- listed private‑credit lenders are showing strain;

- parts of the software and technology‑enabled universe are under pressure;

- oil prices have added another obstacle to an easy policy path; and

- Liquidity structures in private vehicles are being tested.

None of this guarantees a systemic crisis. It does, however, reinforce the argument made in previous Unicorn articles: that long periods of easy money can create fragilities which only become visible when conditions change.

For investors and advisers, the focus should be on process rather than prediction. Liquidity awareness, valuation discipline, genuine diversification and a robust market-scenario framework all help portfolios navigate a world where the illusion of stability in some areas may yet give way to more realistic pricing.

In that sense, the story of unicorns – from unlisted tech valuations to private equity, private credit and now sector‑specific strains – is less about saying “we were right” and more about illustrating why a structured, forward‑looking approach remains essential as the cycle evolves.