Podcast: Building an outperforming equity portfolio for all environments

Join Wehmeyer Ferreira (COO, Systematic Solutions) and Rademeyer Vermaak (Head of Systematic Solutions) as they discuss how the top-performing STANLIB Enhanced Multi Style Equity Fund and the STANLIB Equity Fund are positioned for success in the coming months.

Opinion: Navigating a Shrinking Stock Universe: Opportunities Amid Challenges

Over the past two decades, the number of listings on the JSE has halved, dropping from over 600 in 2001 to fewer than 300 today. This trend is not isolated; globally, the World Bank reports a similar decline in US-listed companies, which have also halved since 1996. With 12 delistings occurring in 2024 alone, investors are left grappling with a pressing question: Does a shrinking pool of stocks hinder our ability to uncover promising investment opportunities and build diverse, out-performing portfolios?

While the reduction in available stocks may seem concerning, it also opens the door to innovation and strategic thinking in investment management. The crux of the matter lies in how we approach portfolio construction and risk management in this evolving landscape.

A word on market cap, liquidity and data quality

One of the most important (and often undervalued) considerations in the portfolio construction process is tradeability. This term refers to the joint nature of a stock’s market cap, as well as its liquidity, which are both important characteristics. Small cap stocks tend to be more illiquid than larger caps, which can have significant trading implications in an investment strategy. Small caps also tend to be more volatile, and are not as well covered by analysts, resulting in poorer quality financial data and earnings forecasts. It should also be noted that the vast majority of delistings and consolidations occur in the mid and small cap space, an area that most prudent strategies avoid due to the aforementioned pitfalls. While opportunities may exist in the tail of the stock market, it is practically only in the large and upper-mid caps, where tradeable, diversified and scalable investment strategies can be built.

Embracing a systematic approach

A systematic investment process can serve as a robust framework for navigating this contracting stock universe.

By implementing a tradeability filter that screens stocks based on their market capitalisation and liquidity, investors can effectively capture around 90-95% of the market’s liquidity, while cutting off most of the illiquid, smaller cap tail. An important distinction is that this filter is dynamic, meaning that instead of trying to capture a static number of stocks which does vary through time (e.g. top 100), we aim to capture a certain percentage of the market’s liquidity and size profile. This filtering process distills the selection universe down to approximately the top 60-70 stocks (with some variation), providing a more manageable and focused investment universe, that is better covered, liquid and with better data quality.

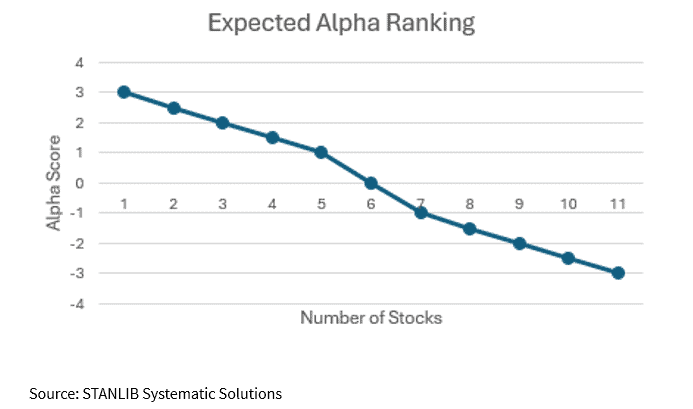

Once this foundation is established, the next step is to delve into key fundamental metrics. By looking at the market cross-sectionally and ranking stocks on a score known as “expected alpha” –which is simply a weighted score across the investment styles of growth, quality and value–investors can pinpoint those with the strongest return potential. This relative scoring system fosters a more nuanced approach to stock selection, shifting the emphasis away from the absolute number of available stocks towards a relative ranking methodology.

For example, consider a hypothetical benchmark of 11 stocks, where each stock has been scored and ranked in a range from -3 to +3. In this scenario, the highest scoring stock has an “expected alpha” of +3, the lowest scoring stock a score of -3 and the average stock scoring 0. In the chart below, you will observe that within this simplistic version of a relative scoring framework, five stocks have a positive score and the remaining five have a negative score. Constructing portfolios using this approach will overweight the positive scoring counters and underweight the negative scoring ones within a portfolio, implying that the absolute number of stocks does not matter. By applying a relative framework, high conviction, active bets can still be made.

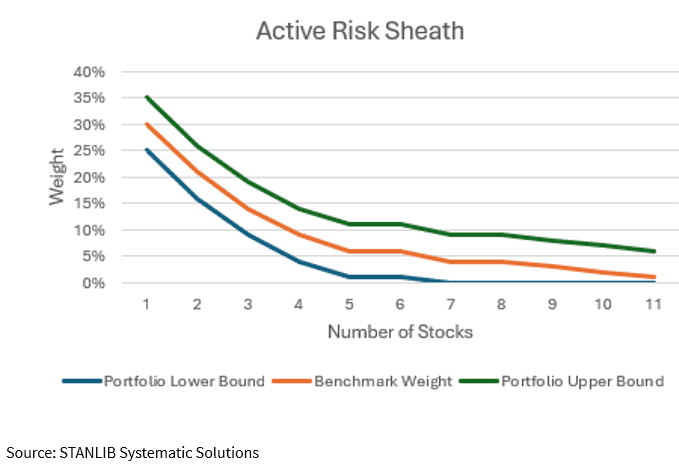

Managing active risk

However, the story is incomplete without understanding risk. Once we have established a view on the expected alpha potential of the various securities, we actively manage the portfolio’s risk. This involves monitoring the degree of variation between our stock and sector positions relative to the benchmark, which we control within a defined range around the benchmark. In our 11-stock universe example, the orange line in the chart below represents the benchmark weight of each security. We set upper and lower bounds on active positioning at both stock and sector levels, allowing us to adjust the width of this range based the fund’s risk appetite. This means that the risk sheath either narrows or widens as needed. In this example, an active position of 5% is allowed, with a lower bound of zero (no holding).

Additionally, we incorporate a layer of macro risk management to control potential unintended macro risks, along with a correlation layer that measures how stocks move in relation to one another. By integrating these components, we can optimise our portfolio construction process to achieve a diversified portfolio with a specific risk profile, even when selecting from a limited number of stocks.

Conclusion

Despite the challenges posed by a shrinking JSE, there are significant opportunities to build truly bottom-up, diversified and active equity portfolios that are robust and capable of performing across various market cycles. Key to this is a flexible process that allows investment teams to dynamically adjust to changing stock attributes and risk changes over time, ensuring that outcomes are consistently optimised for clients.