Key Takeouts

- Global growth remains resilient despite multiple shocks. Strong corporate earnings, fiscal support and continued AI-related capital expenditure have helped markets recover and remain constructive.

- Inflation is limiting central bank flexibility. Inflation risks remain elevated. A changing policy approach at the US Federal Reserve could create more volatility and tighter global financial conditions.

- Liquidity is deteriorating beneath the surface. AI-related investment themes continue to drive capital flows, but this tension is unlikely to persist indefinitely.

- Markets are increasingly dependent on a narrow group of winners. AI and semiconductor-related companies are driving an outsized share of returns. This concentration makes markets more vulnerable.

- Portfolio diversification and active risk management are becoming more important. Investors should avoid over-concentration, broaden equity exposure beyond crowded AI trades, remain selective across asset classes and build portfolios that can withstand a wider range of outcomes.

At the start of 2026, the market backdrop appeared broadly constructive. It was supported by resilient growth, fiscal policy and a strong capital expenditure cycle. That view changed abruptly at the end of February, when the escalation of conflict in the Middle East raised the prospect of a more fundamental regime shift. As we argued in our previous update here, higher energy prices, renewed price pressure and reduced central bank flexibility created a materially more complex environment for risk assets.

Since then, the year has been uneven and more volatile than many expected. The more disruptive regime-shift outcome feared in March has not fully materialised, helped by an easing in energy markets, continued strength in AI-related capital expenditure and more resilient-than-expected global growth. Markets recovered through much of the second quarter and, in some cases, moved back towards new highs, supported by improving macro conditions and stronger-than-expected corporate earnings.

Recently, however, volatility has picked up again. June was less about clear direction and more about renewed uncertainty, as markets continue to grapple with many of the same questions raised earlier in the year: whether growth can remain resilient, whether policy expectations are too benign, and whether increasingly narrow leadership can continue to carry broader asset prices. The result is a market backdrop that is still constructive in important respects, but is also more uneven and increasingly dependent on how underlying risks evolve.

Where are markets now? A lens-based view

Our process begins with an assessment of where markets currently stand, using a consistent set of lenses that capture different dimensions of the cycle. While we do not expect each lens will point in the same direction at all times, the interaction between them helps to frame both opportunities and risks.

Today’s backdrop is defined less by one dominant warning sign and more by the gradual weakening of several market supports.

Economics: resilient growth, but an inflation constraint

From an economic perspective, the global situation is showing more resilience than many would have expected, given the events of the past four months. Growth has slowed in some regions, and expectations have been revised lower in parts of the developed world, but the broader picture is still one of positive nominal growth, continued fiscal support and robust earnings in several areas of the market. Corporate profitability, particularly in parts of the US and across AI-related infrastructure, has stayed stronger than feared.

At the same time, the policy framework has become more complicated. Labour markets are still firm, energy remains a source of uncertainty and the current capital expenditure cycle – particularly spending on AI and related infrastructure – is adding to near-term demand in ways that can keep price pressures firmer than markets expected earlier in the year. In time, that same investment cycle may prove disinflationary if it delivers the productivity gains investors expect, but those benefits are unlikely to arrive in a straight line.

This matters, because central banks are no longer operating in an environment where they can respond freely to any softening in growth. Instead, they are increasingly sensitive to persistent price pressures and to the risk that financial conditions may need to stay tighter for longer. An additional source of uncertainty has emerged from the change in leadership at the US Federal Reserve (Fed). Under Kevin Warsh, the policy framework is expected to place greater emphasis on long-term price stability, while reducing reliance on forward guidance and formal communication tools such as the dot plot and central economic projections.

While this approach may help to anchor long-term expectations, it also leaves markets with less explicit signalling from the world’s most important central bank. In practice, that means greater reliance on incoming data, more interpretation by markets themselves, and potentially a more volatile path for policy expectations and asset prices.

A shift in the Fed’s policy framework also has broader implications for global markets. A more restrained approach to forward guidance and a stronger emphasis on inflation credibility could contribute to a more structurally firm US dollar and tighter global financial conditions. In that context, expectations of a sustained weakening in US exceptionalism may prove premature, even as other regions benefit from cyclical improvements.

Growth continues to support risk assets, but policy flexibility is more limited than it appeared at the start of the year.

Liquidity: still elevated, but moving in the wrong direction

Liquidity continues to be one of the defining features of the current cycle, but the direction of travel is becoming less favourable. In aggregate, global liquidity conditions are still elevated in absolute terms. Fiscal policy continues to provide a degree of offset to monetary tightening, and balance sheet dynamics in some regions are supportive. This helps to explain why markets have been able to absorb shocks and continue to perform, even though policy has become more restrictive in headline terms.

However, the rate of change in liquidity is deteriorating. In a number of major economies, liquidity indicators have rolled over in recent months, and leading signals suggest further softening ahead. Importantly, this deterioration has not yet fully translated into weaker market performance, which in itself is a notable feature of the current environment. Strong thematic drivers – most notably the rise in agentic AI and the related capital expenditure cycle – have, for now, been sufficient to outweigh the trend towards weaker liquidity. This tension is unlikely to persist indefinitely without either liquidity deteriorating further or market leadership broadening.

From a portfolio perspective, this supports a more selective approach to risk assets. In a world where liquidity is deteriorating in many countries, the tolerance for concentration, crowded positioning and weak asymmetry should be meaningfully lower.

A further development worth noting is the re-emergence of large-scale equity issuance. After several years in which major technology companies were significant net buyers of their own shares, the cycle is shifting. A number of large-cap and AI-related companies are increasingly tapping equity markets to fund ongoing capital expenditure.

While this reflects strong demand for investment and the scale of the current capex cycle, it also represents a potential headwind for broader equity markets. Increased supply is likely to require reallocation within portfolios, and historically, periods of elevated issuance have often coincided with later-stage phases of the cycle.

Momentum: still dominant, but increasingly narrow

Momentum has been a powerful driver of markets over the past year, and it continues to hold in many areas. Equity indices in several developed markets (DMs) are still trading close to highs and longer-term trends are supportive. Even so, the quality of that price momentum has changed. Leadership has become increasingly concentrated, with a relatively small number of sectors and themes accounting for a disproportionate share of returns.

The most obvious example continues to be the AI and semiconductor ecosystem, where strong earnings growth and substantial capital investment have reinforced already positive trends. This area has delivered exceptional performance, but it has also become disproportionately important to overall market direction in both DMs and increasingly in emerging markets (EMs), via the semiconductor-dominated Korea and Taiwan indices, now the two largest country weights in the EM index.

This concentration creates a more fragile form of price momentum. The greater risk is that expectations become too elevated, valuations too stretched and markets too dependent on a limited set of outcomes. In that environment, momentum can persist for longer than expected, but it can also reverse more abruptly if conditions change.

Momentum continues to be supported by both price trends and underlying fundamentals. Corporate earnings have been a key positive surprise this year, particularly in the US, where first-quarter results were notably strong, supported by broadly positive management guidance. Current consensus forecasts still imply robust earnings growth continuing into 2027, with elevated margins expected to further expand across several sectors despite a more complex macro background.

This creates an important offset to valuation concerns. Strong and improving earnings help to justify higher multiples, particularly in areas linked to structural growth themes. At the same time, sustained margin expansion reinforces some of the policy constraints discussed earlier, as it suggests that pricing power persists in parts of the corporate sector and that productivity gains, particularly in the US, are likely to continue as AI adoption broadens across industries.

Valuations: a blunt tool, but increasingly relevant for risk

Valuations, particularly in equity markets, are not reliable timing tools. Strong trends and powerful structural narratives can sustain high multiples for extended periods, as has been the case in the current cycle. Conversely, valuations do still influence the distribution of outcomes.

The challenge is that the strongest momentum often sits in the part of the market where expectations, valuations and positioning are already most extended. This creates a less favourable asymmetry. If the growth and earnings outlook continues to deliver, there is still upside potential. But if any of the supporting assumptions weaken – whether through inflation, policy, liquidity or earnings disappointments – the downside can be more meaningful because expectations are already high.

Beyond these crowded areas, the picture is more mixed. There are still regions, sectors and asset classes where valuations are supportive, particularly in parts of EMs, select DM sectors such as financials, and in fixed income, where real yields are more attractive than they have been for many years.

Among commodities, gold continues to play an important role as a geopolitical and diversification hedge. Yet, its behaviour in the current cycle has become more complex, particularly given its increasing correlation at times with South African equities, bonds and the currency. In an environment where real yields are rising and the US dollar may stay firm, the risk-reward profile is less straightforward than earlier in the cycle would suggest, reinforcing the need for active position management rather than static allocation.

The key point is that valuations should not be viewed in isolation, but rather in conjunction with momentum, liquidity and macro conditions to assess where risk is being adequately compensated.

Sentiment and volatility: calm indicators, underlying uncertainty

One of the more notable features of the current environment is the relative calm in many traditional risk indicators, despite the volatility experienced in underlying narratives.

Equity and bond market volatility, while having picked up episodically, is relatively contained rather than stressed. Credit spreads are still tight and in several areas market pricing suggests a degree of confidence in the outlook. However, there are increasing signs of underlying fragility.

Stress in parts of the credit market, particularly in more leveraged and private segments, has been building (an important topic we recently wrote about here). The dispersion of returns across sectors and regions has increased, and market outcomes are becoming more binary in nature. Events such as the March sell-off demonstrate how quickly conditions can shift when several factors move simultaneously.

Under these circumstances, low volatility should not be mistaken for low risk, but regarded as an opportunity to reassess and manage exposures while conditions remain relatively benign.

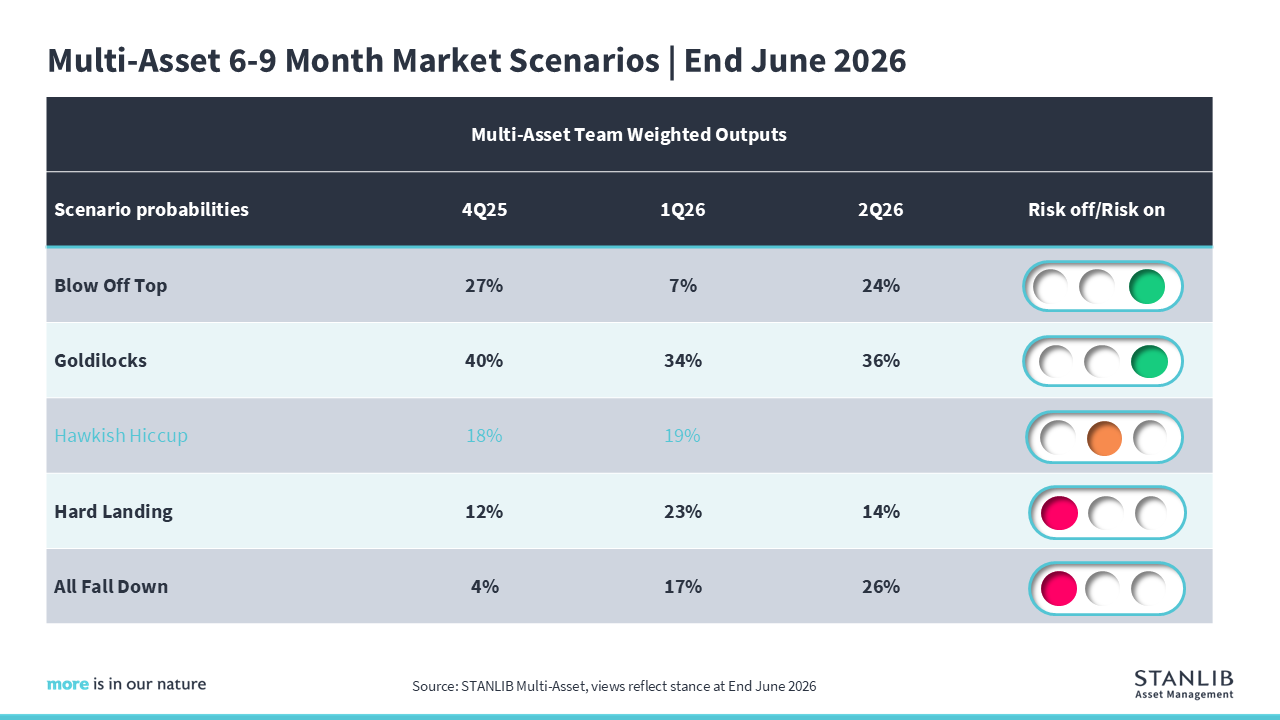

Where could markets go? The scenario framework

Against this backdrop, our forward-looking scenario analysis reflects a more balanced distribution of outcomes than earlier in the year. The team’s latest assessment assigns the following probabilities:

In aggregate, this still implies a higher probability of constructive outcomes than negative ones. The macro and earnings setting is supportive, with structural drivers, such as AI-related capital expenditure, continuing to underpin markets.

The Goldilocks outcome, where market leadership broadens beyond AI-related themes (both regionally and sectorally), is still plausible and is the team’s highest individual market scenario probability. Similarly, the Blow-off top scenario, driven by continued momentum in AI-related themes and capital flows into a narrow set of assets, is still relevant.

At the same time, the risk of more negative outcomes has increased. Scenarios in which inflation proves more persistent, liquidity deteriorates further or market concentration unwinds now form a meaningful part of the overall distribution.

This shift reinforces the idea that markets are no longer operating in a one-directional world. Several outcomes are possible, and the path towards them may be less smooth than earlier in the cycle. The key difference between the two negative market scenarios is that “All fall down” would look more like 2022, when DM government bonds failed to provide their usual diversification against falling equities, whereas a recession-led “Hard landing” would be more likely to restore that relationship.

This reinforces the need to construct portfolios for a number of potential paths, rather than anchor them to a single central case.

Translating this into portfolios

The combination of resilient growth, persistent inflation, deteriorating liquidity and concentrated market leadership has made portfolio construction more challenging in 2026 than in recent years.

Year-to-date, this has been evident not only in market behaviour, but also in the experience of active strategies across asset classes. In several instances, performance was driven less by broad market direction and more by positioning relative to a narrow set of dominant themes. Being even modestly those themes – whether in sector exposure, duration or commodity positioning – has had an outsized impact on outcomes, even where the broader market backdrop has remained constructive. This is an important context for interpreting both market performance and portfolio returns.

From our perspective, it reinforces the importance of process. Our approach is built on assessing how signals across different lenses evolve and positioning portfolios to participate in positive scenarios, while maintaining resilience against alternative outcomes.

In practice, this has prompted a number of clear portfolio actions:

- Maintain exposure to global equities, but broaden beyond the most concentrated parts of the market

- Reduce exposure where momentum and positioning appear most crowded and valuation support is limited

- Increase selectivity within equities, including second- and third-order beneficiaries of the capex cycle

- Manage duration carefully in fixed income, recognising both attractive real yields and the risks around curve dynamics

- Remain cautious in credit, with an emphasis on quality and liquidity

- Actively manage exposure to commodities and gold, recognising their evolving role within portfolios

Importantly, risk management has become more central. In a setting where correlations can shift and shocks can propagate quickly across asset classes, portfolio outcomes are increasingly driven by how exposures interact, rather than by any single high-conviction view.

Position sizing, diversification and the ability to adjust exposures dynamically have therefore become critical components of the investment process.

Conclusion

The current environment is resilient, but it is becoming more complex. The global economy has shown a degree of resilience that would have been difficult to predict at the start of the year, particularly given the scale of the geopolitical and inflation shocks that have occurred. Still, some of the conditions that have supported markets – including liquidity, valuations and policy flexibility – are becoming less favourable at the margin.

This points to a narrower and more demanding path forward. Markets can continue to perform and the cycle still offers opportunities, but the balance of risks has shifted and the range of plausible outcomes has widened.

Under these conditions, the objective is to take risk where it is appropriately compensated and to remain selective where asymmetry has become less favourable. That, ultimately, is the role of a disciplined multi-asset process: to navigate changing probabilities with flexibility, consistency and clear portfolio discipline.