Key takeouts:

- The perceived “stability” of private assets is largely an illusion (unless in the hands of experienced and effective managers): it is the result of infrequent pricing and limited transparency.

- Private equity and venture capital distributions have collapsed, while secondary market sales are surging at steep discounts.

- Private credit is facing rising defaults and hidden risks, despite the appearance of smooth returns.

- In private markets, the gap between winners and losers is wide — and difficult to see before it’s too late.

- Our multi-asset team manages flexible, listed portfolios, well-equipped to respond to uncertainty. Our expert teams managing private assets are leaders in their fields and emphasise discipline, liquidity, transparency and robust risk management. This approach ensures consistent and credible investment returns for clients who are aware of illiquidity risks and have time horizons aligned with their goals for “return of capital,” not just “return on capital.”

Introduction: The Calm Before the Recognition

In 2019, we cautioned clients that the boom in “unicorn” companies – private businesses valued at over $1 billion – was not being driven by grounded fundamentals but by cheap money, hype and opaque valuations. At the time, venture capital and private equity funds were aggressively bidding up assets based on growth stories, not profits. In 2023, we returned to that theme, warning that the Covid-era flood of capital had inflated already-fragile foundations.

In 2025, the risks we raised have begun to surface. While most headlines have focused on the struggles of high-profile tech start-ups, the real issues run deeper. They affect not just venture capital (VC), but also private equity (PE), private credit, and the very assumptions many investors hold about private assets. The need to fully understand the potential risks of the underlying assets and select experienced managers, such as our private markets team, has become even more important.

The problem is not that these investments are inherently bad. It’s that many were sold as low-volatility and low-risk, simply because they are not priced every day, like listed assets. In reality, that “stability” is often an illusion, created by the so-called “mark to model” approach, where fund managers value their own assets, often with limited external validation (a practice sometimes referred to as “marking their own homework”). Risks are there – especially around liquidity – but often remain hidden until forced to the surface.

In this article, we unpack how the structure of private markets masks risk, the pressure building under the surface, and why we believe diversified, liquid, and flexible portfolios – like the ones we manage – are more critical than ever.

From Rarity to Herd: The Oversupply of Unicorns

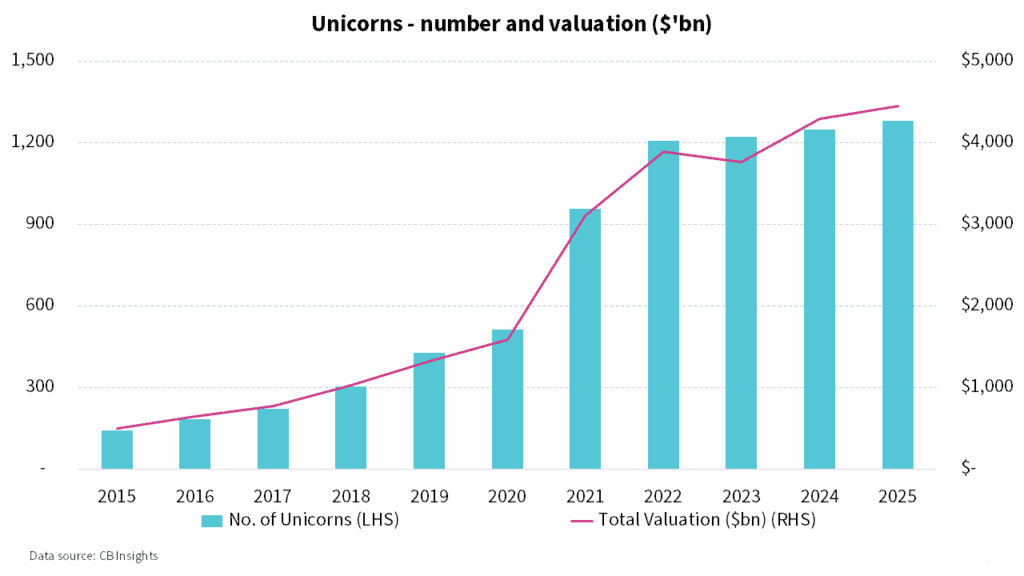

Not long ago, the term “unicorn” reflected something special: a private company valued at over $1 billion. There were fewer than 50 of them in 2013. It was rare, exciting and usually implied a disruptive business model. But between 2019 and 2022, the unicorn population more than tripled, from around 400 to over 1 200 globally – with combined valuations rising from $1.3 trillion to approximately $4 trillion.

This was not because three times more world-changing businesses were suddenly founded. It was the result of too much capital chasing too few ideas. Venture capital funds were flush with cash, interest rates were close to zero, and investors feared missing out on the “next big thing”. As a result, many companies achieved billion-dollar valuations before they had profits – and in some cases, before they had meaningful revenue.

Then came the reversal. As rates rose and liquidity dried up, the pace of new unicorn creation had collapsed by over 90% by early 2023. More importantly, many of the companies that had raised capital at inflated valuations could not sustain them – leading to down rounds (where new funding was raised at a lower price) or failed attempts to go public (not just a private market issue – Beyond Meat, for example, is a public case study of valuation collapse).

Figure 1: Global Unicorn Count and Combined Valuation

The Great IPO Let-down

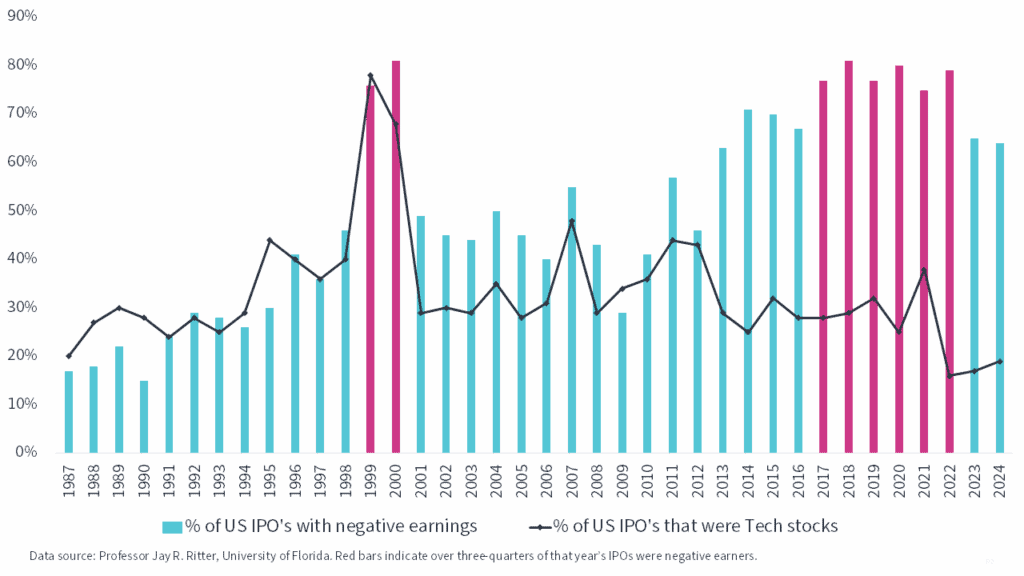

A key assumption behind the venture capital model is that successful companies will eventually go public, offering investors an exit and a liquidity event. But the initial public offering (IPO) market has become far more selective.

From 2020 to 2022, nearly 80% of US IPOs were companies that were still unprofitable at listing. In a low-rate environment, that was acceptable – investors were willing to wait for profits. But in today’s market, patience has worn thin. Companies with large losses and no clear path to positive cash flow are now facing a very tough audience.

By late 2024:

- IPO volumes remained well below pre-pandemic levels.

- Valuations were routinely cut by 30–70% from their last private round.

- Many unicorns delayed going public entirely to avoid a public repricing.

In short, the pipeline from VC to IPO has narrowed. And with no profitable exit, the entire model of “grow fast, exit big” is now under pressure. This raises a deeper question: if higher rates alone can trigger such dramatic valuation losses, was durable value ever being created? Shouldn’t this risk have been understood and priced in by experienced managers?

Figure 2: % of US IPOs with Negative Earnings

The Private Equity Liquidity Crunch: What Clients are not Being Told

PE has long been a favourite among institutional investors – especially large endowments, pension funds, and family offices. The pitch was simple: higher returns in exchange for locking up capital for 7–10 years. But that trade-off only works if investors eventually get their money back and if valuations are based on sound fundamentals, not overly optimistic assumptions.

And that’s where the system is now under stress.

How Private Equity Cashflows Actually Work:

When investors commit money to a PE fund, they do not send the cash upfront. Instead:

- The fund manager (called the GP, or “general partner”) makes “capital calls” — drawing down money in chunks over time to invest.

- Later, the manager sells companies (via IPO or private sale) and returns capital to investors. These are called “distributions”.

- The investor (the LP, or “limited partner”) only earns real returns when these distributions start to exceed the original commitment.

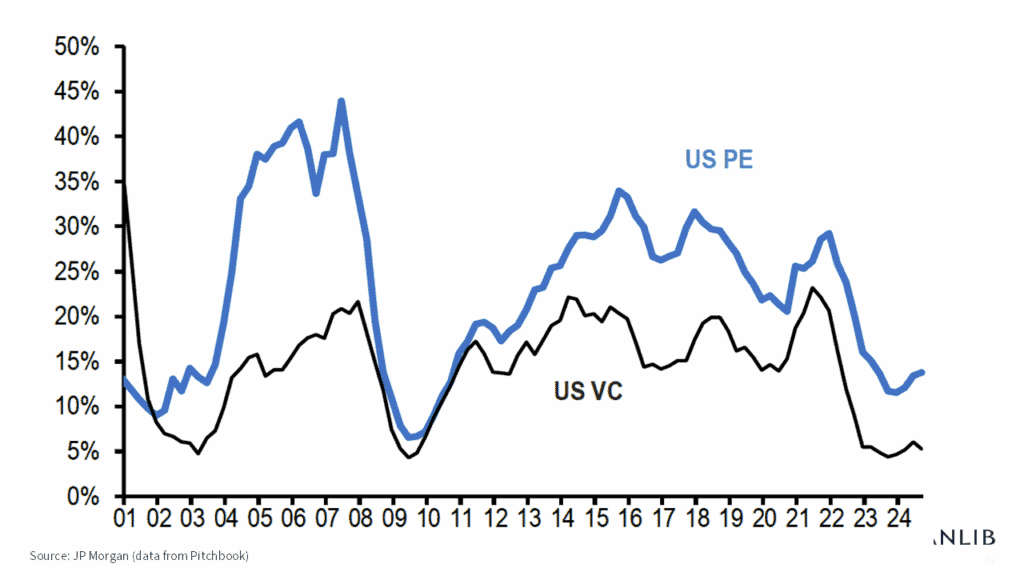

But in 2023 and 2024, the system jammed:

- Capital calls continued (new investments still being made).

- Distributions fell sharply, reaching their lowest level as a percentage of assets since the Global Financial Crisis (GFC).

- Many investors became cashflow negative – more money was going out than coming back in.

Even elite investors felt the squeeze. Harvard and Princeton began selling stakes in old PE funds on the secondary market to raise cash. The reason? Too much capital stuck in illiquid assets, and not enough coming back.

Figure 3: Rolling 12-month US PE and VC Distributions as % of Net Asset Value

The Secondary Market Surge – and What it Really Means

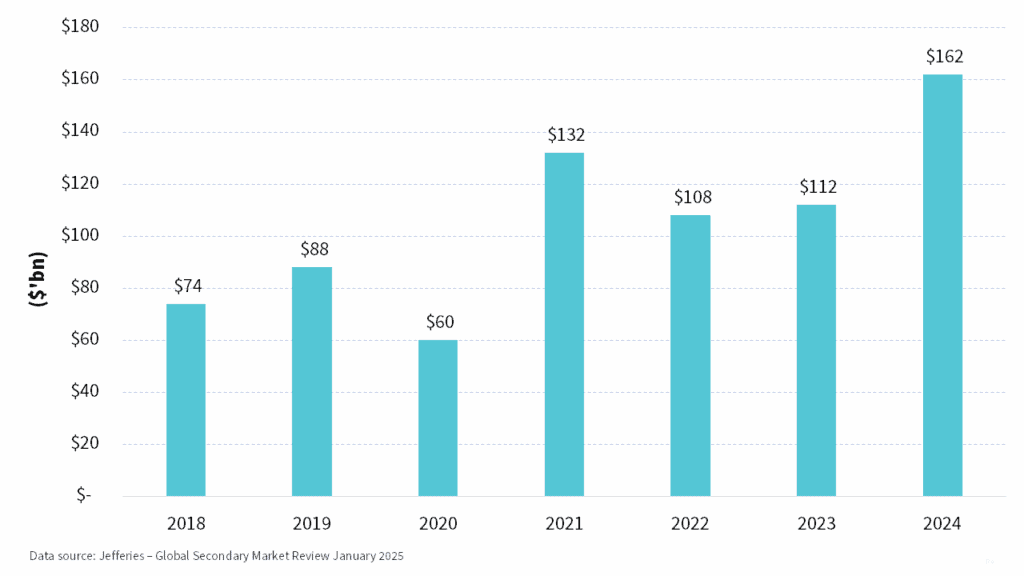

When private investors are unable to get their money back through normal distributions, the only option left is to sell their positions – even at a discount.

That’s where the secondary market comes in. It allows investors to sell their stakes in PE and VC funds to other buyers. But, unlike public markets, these sales happen privately, slowly, and often at a significant discount to the last reported value – reflecting a wide gap between modelled pricing and actual market demand.

In 2024:

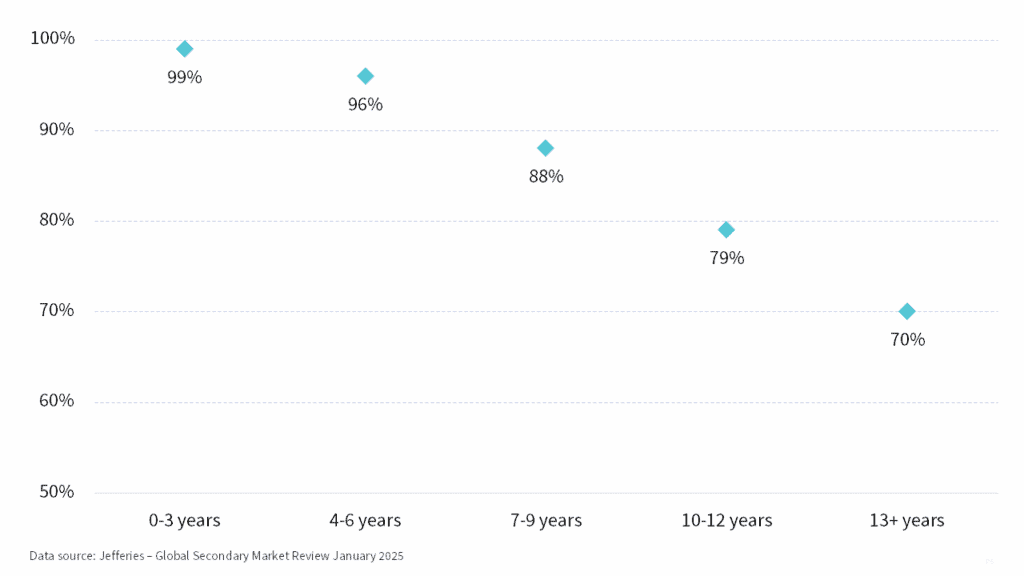

- Global secondary market volume hit a record $162 billion, but much of it was at significant discounts to NAV.

- Early-stage VC funds traded at 31–41% discounts, growth PE at 12–25% and private credit funds at 14–24%, according to Lazard.

- More than 40% of sales came from funds less than six years old — suggesting investors were not just trimming legacy exposures but actively retreating from recent vintages too.

Figure 4: Secondary Market Fundraising per year ($’bn)

Why does this matter? Because these discounts tell us something the official NAVs do not: buyers believe many private assets are still overstated in value. In other words, investors selling these stakes are saying: “We know we’re not going to get full value, but we’d rather take 75 cents on the dollar now than wait years for a maybe”.

What’s causing the discounts?

- Unrealised valuations: GPs often value companies based on old funding rounds or internal models, not on what they would sell for today.

- Lack of exits: No IPO = no cash = no ability to return money.

- GP-led “solutions”: Fund managers are increasingly creating vehicles to sell their own assets to themselves — so they can avoid writing them down.

This last point deserves special attention. Known as “continuation vehicles,” they are marketed as liquidity solutions, but often look more like a shell game, where fund managers move hard-to-sell companies into new funds, reset timelines, and raise new fees, all without exposing these assets to real price discovery.

Figure 5: 2024 Average Buy-out Pricing by Age of Fund (% of Net Asset Value)

Another emerging development highlights just how far some managers are reaching to create exit opportunities, even if it means passing risk onto uninformed buyers. In May 2025, reports surfaced that the US administration was considering opening 401(k) retirement accounts to private equity investments. While marketed as democratising access, some industry insiders have warned that retail investors risk being saddled with illiquid, overvalued, or hard-to-sell assets, especially if professional investors are increasingly using the secondary market to offload them at a discount

Private Credit: Yield Without Risk? Think Again

Private credit – where funds lend directly to companies rather than buying bonds – has grown rapidly over the last decade, partly as banks stepped back due to post-GFC regulations. While many investors were drawn by the promise of high, floating-rate returns, it is worth remembering that credit quality still matters and valuation risks are not absent. Still, unlike equity investments, private credit often comes with contractual maturity and repayment structures, which can offer a clearer path to realising value.

But, as always, return = risk. And now, those risks are surfacing.

According to Fitch:

- The default rate in private credit hit 8.1% in Q4 2024 — the highest ever recorded.

- Some large deals struck in 2020–21 are already being restructured or extended.

- Lenders are using all kinds of tactics to avoid recognising losses, such as:

- “PIK toggles” (paying interest with more debt instead of cash)

- Extending maturities without proper repricing

- Valuing impaired loans above what public markets would pay.

What’s the trick?

Private credit funds are not marked daily. Managers set their own NAVs using internal models. Unless a borrower formally defaults, managers often do not mark the loan down – even if the borrower is clearly distressed.

In public markets, if a bond drops 20% in price, it shows up immediately. In private credit, that same bond can sit at par for months — giving investors the illusion of safety.

And unlike PE or VC, most private credit funds promise regular liquidity (monthly or quarterly redemptions). But if too many people try to exit at once, funds can gate withdrawals – something we saw with several non-traded REITs and private credit vehicles in 2022–23.

So far, most investors have not noticed because reported returns remain positive. But we believe this is a mirage. If conditions tighten, many of these vehicles will be forced to reprice and investors could be stuck with both losses and no access to their capital.

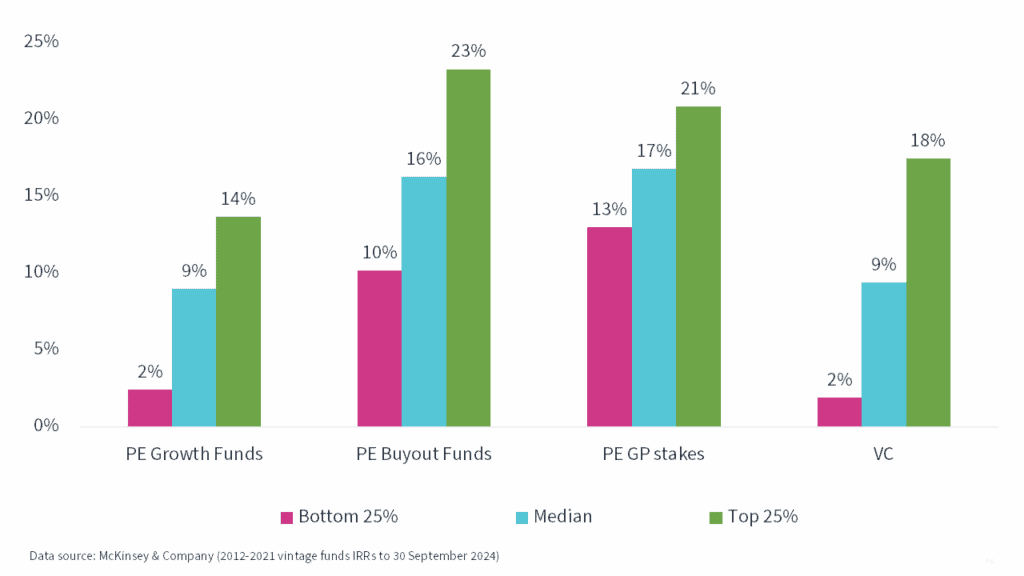

Not one Market – But Many: Dispersion and the Manager Trap

Private assets do not only carry illiquidity risk. They carry dispersion risk — the huge gap between good and bad managers:

- In public equities, the spread between top and bottom quartile funds is typically 2–4% per year.

- In PE, the spread between top and bottom quartile managers often exceeds 12–15% IRR, and in VC it can be well above 15%, depending on strategy and vintage.

- In private credit, early 2020s vintages are already showing wide performance divergence, depending on loan quality and sector exposure.

This means that manager selection – and vintage year timing – matters more in private markets than almost anywhere else. Unfortunately, many investors have limited transparency into what they are buying. Documents are dense, reporting is quarterly at best, and performance data is often cherry-picked.

In the last cycle, strong returns were more about beta — everything went up. Going forward, it’ll be about alpha — and avoiding the landmines.

Figure 6: Private Equity Strategies Exhibit Wide Return Dispersions

Final Thoughts: Volatility Deferred can be Destructive

Since 2019, we have been urging clients not to confuse delayed pricing for low risk. Many private asset managers have simply been kicking the can – delaying write-downs, extending holding periods, and hoping for a return to the easy-money era.

We are not saying private markets are broken. They could still play a role in diversified portfolios. But the narrative of smooth returns, no volatility, and superior performance is being unmasked. Much of what looked “low risk” was simply not being marked down yet.

What do we recommend?

- Stay diversified across liquid assets – they offer the flexibility to respond when conditions change.

- Be highly selective in private allocations – focus on managers with real discipline, not just a glossy pitch.

- Size exposures based on actual liquidity needs, not theoretical valuations.

- Do not buy into the myth of “volatility-free” returns.

In a world of rising dispersion, illiquidity, and delayed price recognition, portfolios built with real-time market inputs are better equipped to adapt and manage risk. Our multi-asset team continues to invest with transparency, liquidity and discipline – not only to deliver returns, but to help clients navigate uncertainty with confidence.

In this environment, agility is not optional — it’s essential.

Sources consulted

A wide range of reports, research materials and articles informed the views expressed in this article. The following public sources are those most directly cited or referenced:

Bain & Co. Global Private Equity Report 2025

CB Insights Unicorn Tracker

Evercore Private Capital Advisory Survey 2024

Financial Times, “Ivy League endowments sell private equity stakes amid buyout downturn”

Financial Times, “Private equity is more stuck than ever — and secondaries will benefit”

Fitch Ratings Credit Journal – Private Credit

Jefferies 2024 Secondary Market Review

Lazard Secondary Market Report 2024

Pitchbook Q1 2025 Venture Monitor

Prof. Jay Ritter’s IPO Statistics