Key points

- Trump’s America First policy is creating a fundamental shift in global power dynamics, leaving regional powers to assert themselves in a multi-polar world.

- The global security environment is deteriorating, with military expenditure rising to an all-time high, driven by increased spending in Europe, Asia, Oceania, and the Middle East.

- This shift is driving European nations to set aside substantial defence spending outside traditional budget norms, creating a multi-year defence opportunity for global defence.

America First

STANLIB Multi-Asset’s pre-election analysis of the November 2024 US presidential election revealed that both candidates favoured increased defence spending, although with a different emphasis — whether to enhance national security or better defend borders against the fentanyl drug crisis. This bipartisan support positioned defence as a potential winner regardless of a Harris or Trump electoral outcome, a view that has proven prescient with the Trump administration’s America First defence agenda.

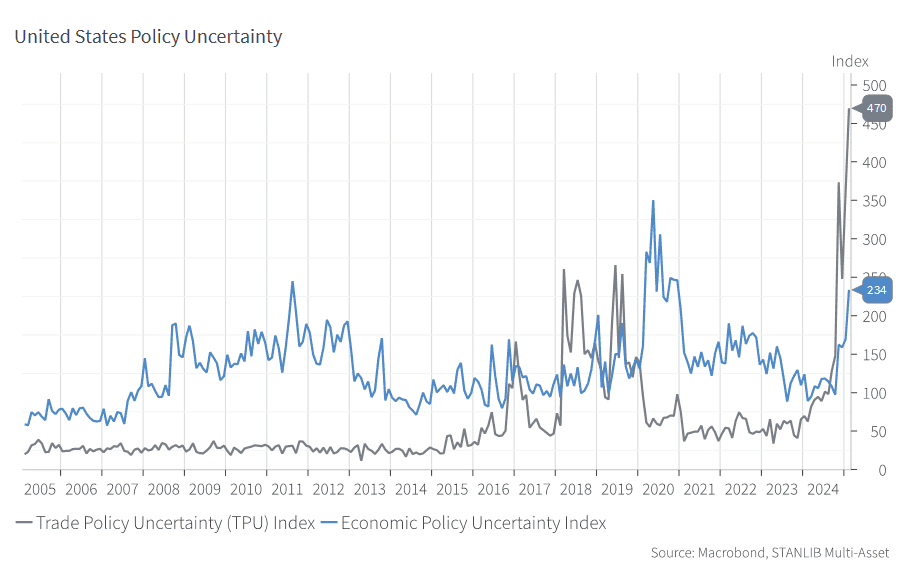

Although initially triggered by America’s political cycle, the trade we implemented in October 2024 was geared towards global, and not just US, defence companies. We developed a custom basket skewed away (at the margin) from the US towards Europe and some parts of Asia. To get a purer defence focus, we minimised noisy aerospace names. We had a large chunk in Europe given the war in Ukraine and the rearmament opportunity. The Multi-Asset team likes trades with asymmetry. In addition, we could see upward kickers for nations to value their defence independence and not be at the mercy of the US election cycle.[i] In our political research, we could see the US policy making under Biden and talk on the campaign trail by Trump was fuelling such a move. Realising defence is going through change, we added emerging defence tech players to the known behemoths. In 2025, we witnessed a rapid increase in geopolitical uncertainty. Figure 1 shows the extent and speed of change of these new highs in policy uncertainty indices.

Figure 1: Rising Uncertainty

America First

STANLIB Multi-Asset’s pre-election analysis of the November 2024 US presidential election revealed that both candidates favoured increased defence spending, although with a different emphasis — whether to enhance national security or better defend borders against the fentanyl drug crisis. This bipartisan support positioned defence as a potential winner regardless of a Harris or Trump electoral outcome, a view that has proven prescient with the Trump administration’s America First defence agenda.

Although initially triggered by America’s political cycle, the trade we implemented in October 2024 was geared towards global, and not just US, defence companies. We developed a custom basket skewed away (at the margin) from the US towards Europe and some parts of Asia. To get a purer defence focus, we minimised noisy aerospace names. We had a large chunk in Europe given the war in Ukraine and the rearmament opportunity. The Multi-Asset team likes trades with asymmetry. In addition, we could see upward kickers for nations to value their defence independence and not be at the mercy of the US election cycle.[i] In our political research, we could see the US policy making under Biden and talk on the campaign trail by Trump was fuelling such a move. Realising defence is going through change, we added emerging defence tech players to the known behemoths. In 2025, we witnessed a rapid increase in geopolitical uncertainty. Figure 1 shows the extent and speed of change of these new highs in policy uncertainty indices.

Figure 1: Rising Uncertainty

The Need for Rearmament

We anticipated that stocks of older equipment donated to Ukraine would need comprehensive replenishment by NATO. This, combined with political pressure to stimulate European economies by keeping defence procurement within EU borders, would create strong tailwinds for European arms manufacturers. These tailwinds may become a gale.

Europe has long relied on America to do the heavy lifting as peacekeeper on the world stage. EU member states spend around a third of the US spend on defence expenditure. This arrangement, comfortable during relatively peaceful decades, has created structural vulnerabilities now exposed by shifting geopolitical realities. US Vice President JD Vance’s watershed speech at the Munich Security Conference in February 2025 has shocked the continent. Further broadsides were Trump’s handling of Zelensky and his willingness to exclude Ukraine from peace talks with Russia. The clear end of the status quo has accelerated European defence autonomy initiatives.

Europe Defence Spending Backlog

The prolonged Russia-Ukraine war, now in its third year, has exposed the weakness of Europe’s defence preparedness, as Trump’s America First doctrine and a potential US pivot to focus on Asia challenge long-standing security assumptions. This situation is compounded by Europe’s depleted ammunition stocks, aging equipment fleets, and reduced manufacturing capacity.

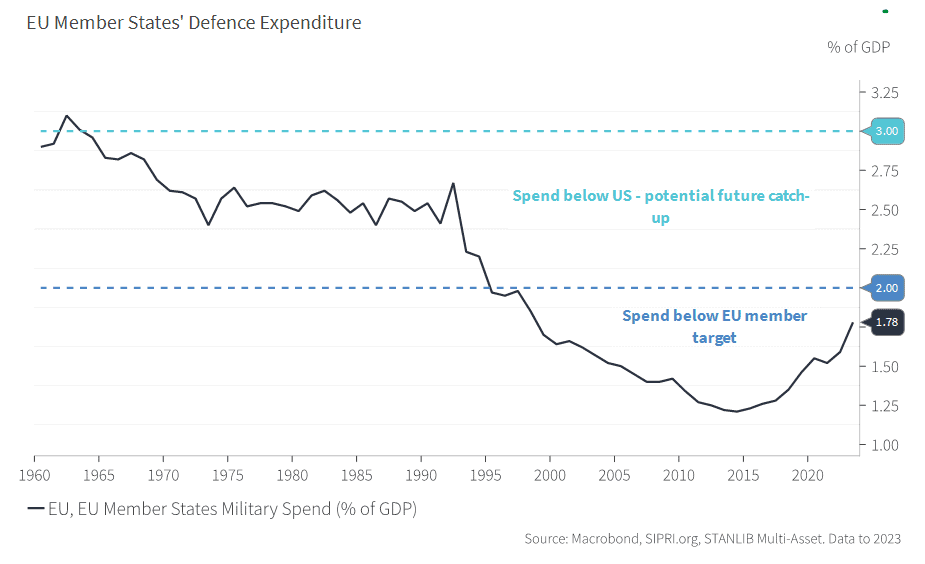

The numbers underpin the stark picture in Figure 2: European NATO members underspent on defence by approximately €300 billion cumulatively over the past decade compared to their 2% GDP commitment. While the average NATO European member spent 1.45% of GDP on defence between 2014 and 2023, the US maintained approximately 3.5% of GDP during the same period, creating a significant capability gap.

Figure 2: Mind The Gap – Europeans’ Long-standing Defence Underspend

Several European countries have publicly committed to raising defence spending targets to 3% of GDP as a base case, notably Poland and the Baltic states. Post-election Germany’s new coalition plans dedicated infrastructure and defence funds of around €400 billion each.[ii] The UK has also signalled intentions to reach this threshold by 2030. While these commitments improve future spending flows, they must address a backlog of decades of chronic underinvestment in critical capabilities.

Draghi’s EU Competitiveness report clearly articulated the challenge: “Nevertheless, the EU’s defence industrial base faces challenges in terms of capacity, know-how and technological edge. As a result, the EU is not keeping pace with its global competitors.”[iii] The recent support from the European Commission to provide €150 billion in loans to boost defence spending and create a mechanism allowing countries to spend an additional €650 billion on defence over four years without triggering budgetary penalties aims to tackle this. European Commission president Ursula von der Leyen agrees, saying: “We are in an era of rearmament.”[iv]

Not fighting the last war

There is an opportunity for recovery as countries look at their defence spending needs. New technologies are reshaping future defence requirements. The war in Ukraine has demonstrated the effectiveness of low-cost drone swarms, with over 10 000 drones deployed monthly in combat operations. Advanced threats like hypersonic missiles, and targeting of critical infrastructure such as undersea data cables, demand new defensive systems and strategies.

Spending better with greater regional coordination would enable more research and development spend, which, despite European Defence Fund support, is lagging other regions’ R&D. We expect more M&A activity to consolidate the fragmented industrial base as products get more standardised, and bring in new technologies.

There are also new initiatives being added to defence shopping lists. Regional missile defence shields, like Israel’s Iron Dome, have entered serious planning stages in both the US and Europe. These systems would require substantial investment to provide multiple protection layers against diverse airborne threats, potentially exceeding €100 billion for comprehensive European coverage over the next decade.

Beyond Europe

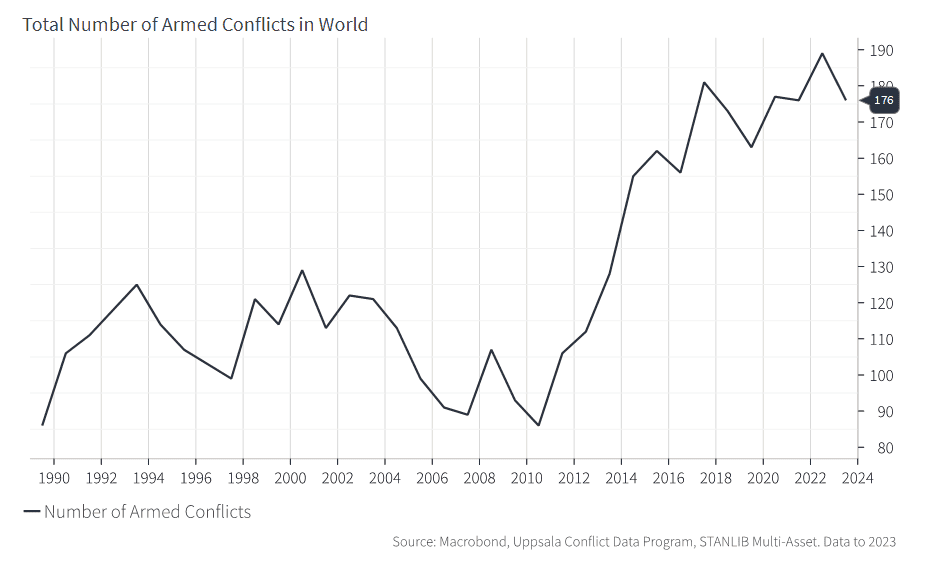

The global security environment is deteriorating more rapidly than public perception acknowledges. Our World in Data currently tracks over 100 active conflicts globally. According to the Stockholm International Peace Research Institute (SIPRI): “In 2023, world military expenditure rose for the ninth consecutive year to an all-time high of $2 443 billion. For the first time since 2009, military expenditure went up in all five of the geographical regions defined by SIPRI, with particularly large increases recorded in Europe, Asia and Oceania and the Middle East.”[v]

Figure 3: Not in a Safer World

Risks

Return of the Peace Dividend

Peace is a potential headwind to this trade, but even with peace, the withdrawal of the US as policeman of the world compels others to make changes in the current geopolitical environment. Trump’s transactional diplomatic style, the large domestic US budget deficit, and his America First strategy are causing the US to step sharply back from subsidising other countries’ security, ending the post-Cold War era where regions like Europe or countries like Taiwan could underspend on defence while relying on American guarantees.

We are witnessing a transition to a multi-polar world where regional powers are asserting themselves with less American oversight. This fundamental shift in global power dynamics requires European self-reliance in security matters. The EU has explicitly outlined defence as a strategic element of its competitiveness agenda and acknowledged that its chronic underspending is causing it to lose ground technologically to rivals. The June 2024 European Commission statement identifying a €500 billion investment gap reflects an institutional commitment that transcends electoral cycles and would be difficult to reverse even if geopolitical tensions temporarily ease.

Political Will to Consolidate

The European defence industrial base remains highly fragmented along national lines, limiting economies of scale and creating inefficiencies. The Ukraine conflict exposed critical interoperability challenges. For example, NATO standard 155mm artillery shells were provided to Ukraine along with ten different howitzer systems from EU member states, while Europe maintains 12 different battle tank platforms compared to America’s single standardised model. This creates logistics and training challenges for the “boots on the ground”. [vi]

The Draghi report and subsequent European Commission statements strongly advocate for consolidation to improve scale, cost efficiency, and innovation capacity. The key question is whether national governments will surrender control of “strategic crown jewel” defence companies to create European regional defence champions capable of competing globally. Recent joint Franco-German projects suggest momentum toward greater integration, which promises a huge medium-term opportunity, though political hurdles remain substantial.

Risk of Overvaluation

European defence sector equities have appreciated significantly year-to-date, raising questions about valuation. However, Bank of America analysis suggests more upside with only 2% of GDP level of increased spending being currently reflected in share prices. Recent research notes that NATO members ex the US were expected to spend around $450 billion on defence in 2024, and every country meeting 2% of GDP would be an incremental $45 billion of spend on defence. Raising the target to 3% this would be an incremental $250 billion. [vii]

The EU defence sector is currently trading at c.11x EV/EBITA in 2027 vs. US peers at 13x. This valuation gap against US counterparts suggests additional upside potential, especially as spending commitments materialise into firm orders and backlog growth.

In our multi-asset process we analyse positions through more than one lens. The valuation and economic drivers were attractive at the outset. Initially, the defence position cost some relative performance post the US election, but we re-underwrote and added to the position. Trump’s actions, and not just idle threats, then accelerated European stock price action, and we have seen a hyped news flow. Sentiment is one of our contrarian lenses. Price momentum was also overextended. Our lens analysis and changes in our scenario probabilities steered us to take some profits (banking profits in a volatile Trump world rather than letting them run in a new regime scenario).

Ironically, our position is smaller as we anticipate some short-term share price consolidation as the European stocks have run quite hard. Yet our conviction is higher, as the political momentum and commitment to defence have strengthened. The structural drivers remain intact, even if markets need a breather to digest recent gains.

Conclusion

Trump’s new America First policy is altering the boundaries and terms of what defence guarantees the US will offer. Countries will have to look to boost their self-reliance in this new world order. The global defence sector presents compelling investment opportunities driven by structural rather than cyclical spending increases. We see this starkly in Europe with a €500 billion investment gap over the next decade, clear political consensus on the need for rearmament, and relatively attractive valuations compared to US peers. European defence contractors offer exposure to a multi-year growth cycle, with spend spill overs to other connected global defence players.

While acknowledging the unfortunate necessity of increased defence preparedness, it bears noting that historically, defence research has generated significant civilian technology spill overs such as carbon fibre composites, LiDAR systems now central to autonomous vehicles, internet communication protocols, and GPS positioning technologies. The current innovation wave in areas like artificial intelligence, advanced materials, and unmanned systems may yield similar dual-use benefits.

As investors seek sectors with both defensive characteristics and growth potential in an uncertain macroeconomic environment, global and particularly European defence represents a thematic opportunity with substantial runway for our clients.

Your clients can access this thinking through the multi-asset funds and portfolios managed by STANLIB Multi-Asset.

References

[i] See President of the European Council, Charles Michel, 19 March 2024 speech: “We can no longer count on others or be at the mercy of election cycles in the US or elsewhere.”

[ii] https://www.reuters.com/world/europe/germany-weighs-special-funds-defence-infrastructure-sources-say-2025-03-02/

[iii] Draghi’s The future of European competitiveness, Part B, pg 159.

URL: https://commission.europa.eu/document/download/ec1409c1-d4b4-4882-8bdd-3519f86bbb92_en?filename=The%20future%20of%20European%20competitiveness_%20In-depth%20analysis%20and%20recommendations_0.pdf

[iv] Bloomberg, 4 March 2025, EU Proposes €150 Billion Defense Loan as Trump Pulls Back

[v] SIPRI.org https://www.sipri.org/media/press-release/2024/global-military-spending-surges-amid-war-rising-tensions-and-insecurity. Bolding our own.

[vi] Source: Draghi Part B, p 164

[vii] Bank of America,3 March 2025, European Defence: Pressure grows on Europe to provide support for Ukraine