Key points:

- Agility and discernment will be essential for generating returns in an unpredictable 2026.

- Despite a strong 2025, markets enter 2026 with supportive liquidity but growing uncertainty around US rate cuts and economic momentum.

- The STANLIB Multi-Asset investment team maintains a selective risk‑on stance, recognising both AI‑driven opportunity and rising geopolitical and structural vulnerabilities.

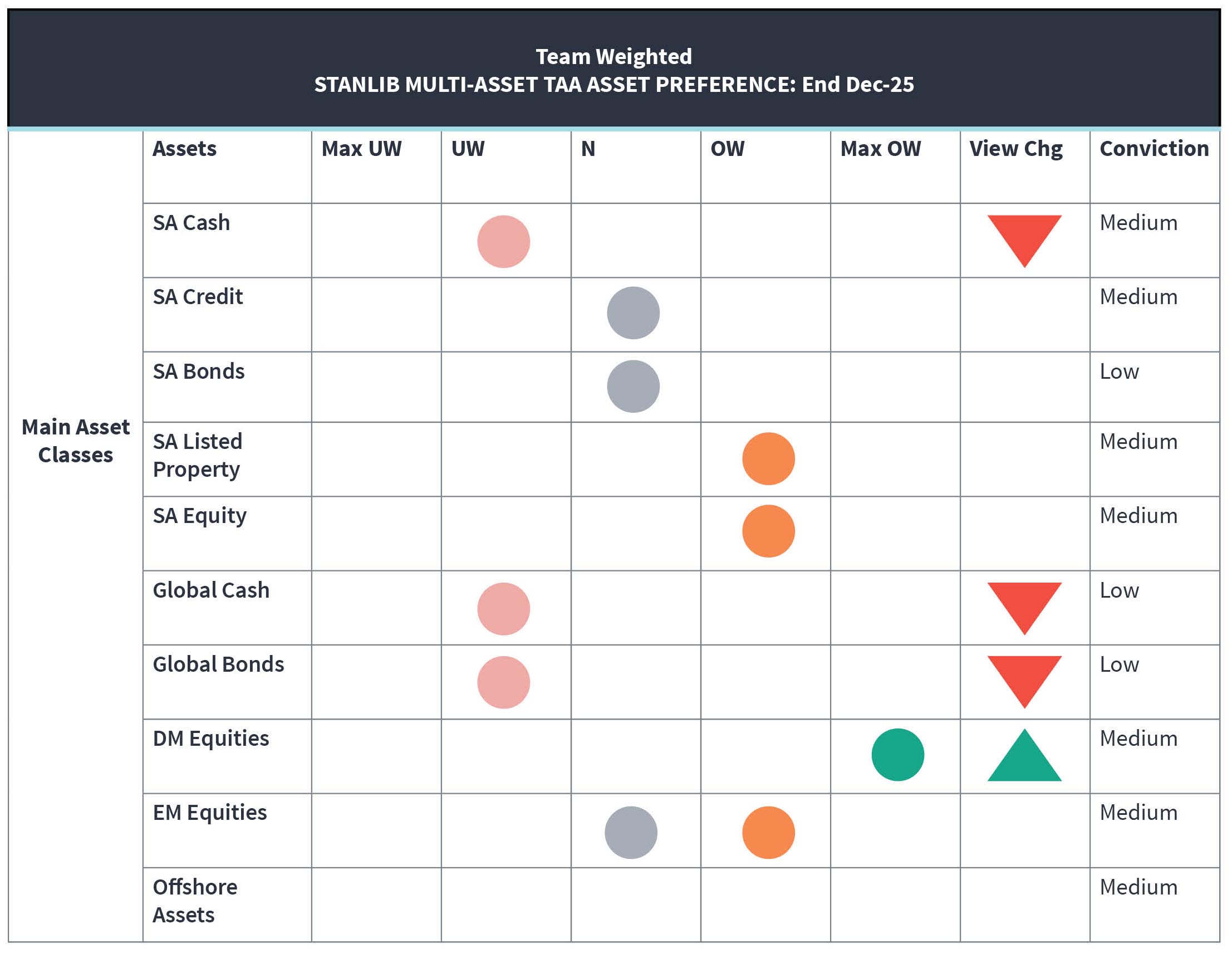

- The team’s positioning favours SA and developed‑market equities over global bonds, with targeted sector and commodity exposures applied through efficient portfolio tools

- In 2026, diversification, flexibility and active management will be critical as policy shifts, inflation risks and global dynamics shape market outcomes.

At the centre is recognition that policy support—both monetary and fiscal—remains a cornerstone for equities. An exceptional period of earnings growth leads us to believe it will continue, for now. This should continue to prove fertile, just as economic growth has proven resilient despite tariffs, geopolitical upheaval and increasing disparities (evident in K-shaped consumption patterns) among other factors highlighted by our Chief Economist, Kevin Lings. These factors are not enough for us (or him) to expect the current cycle to be derailed. In fact, we have an active working hypothesis for “early cycle” thinking to be part of our investment outlook, if not a major differentiated perspective.

We believe the liquidity environment is very supportive. There is increasing fiscal support, and a continued monetary policy environment that points to further interest rate cuts around the world, although that rate cutting cycle policy support will lessen over the next 6-9 months (our tactical horizon). Growing risks in fixed income are raising questions about the safety of fixed income assets – a point we have always made (“all assets are risk assets”).

Our risk appetite, while bullish (we were called nervous bulls in 2025) is tempered by an awareness of numerous structural and cyclical vulnerabilities that could require us to adjust quickly. Themes such the transformative role of artificial intelligence (AI), and reform-driven opportunities in markets like SA, South Korea and Japan, are front of mind. Conversely, geopolitical tensions around the globe are increasing, strategic alignments are breaking down and evidence continues to highlight the smashing of the “old rules”. This reinforces our team’s belief that optical diversification is not sufficient in current portfolios and flexibility in outcomes and actions are essential tools for navigating the increasing risks and (as is always the case) uncertainty about what lies ahead.

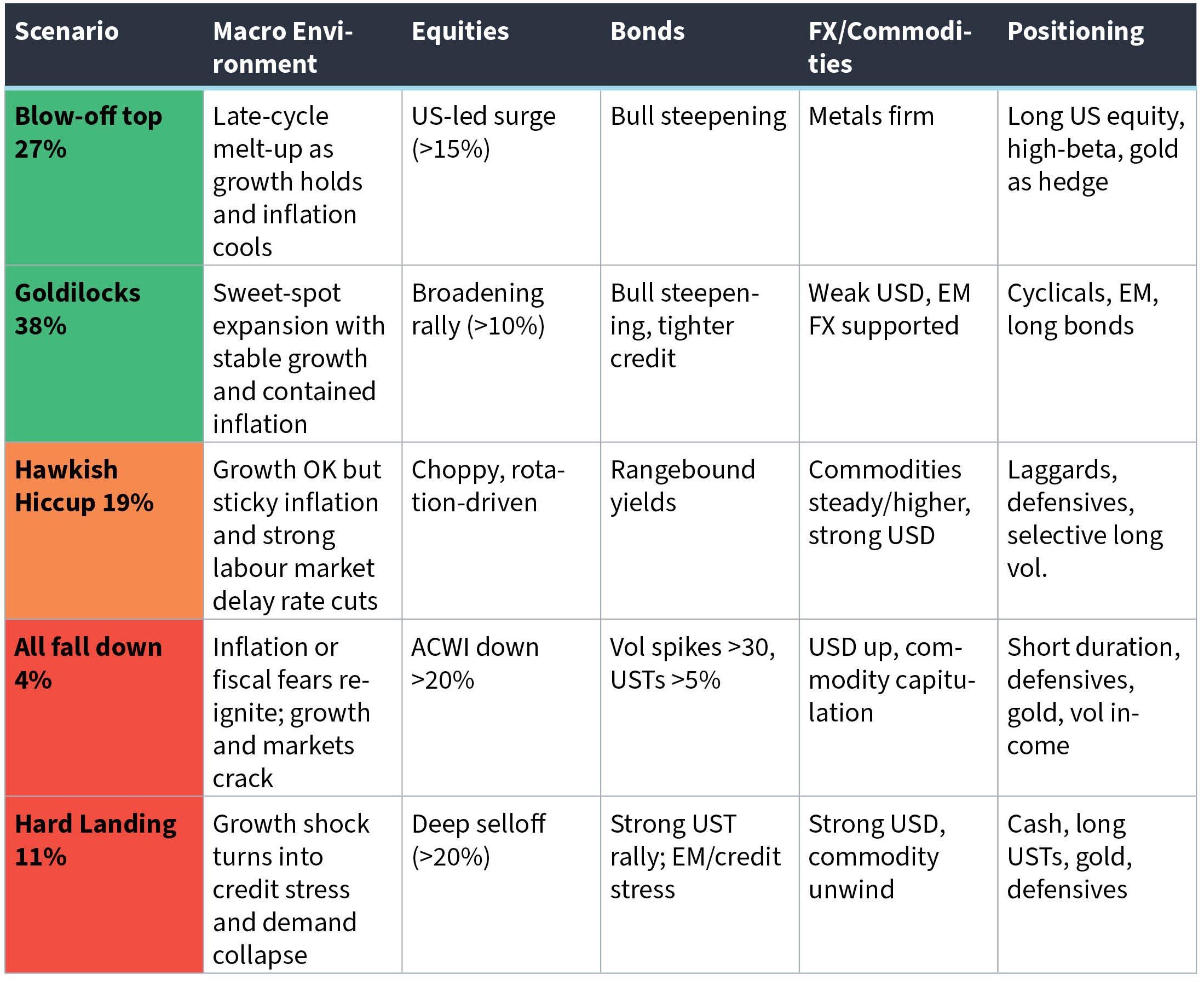

In our market scenario probabilities, the team’s bearish outlooks, which were low anyway, have increased, while highlighting a new amber risk, especially given current consensus views about the path of interest rates in the US. A less dovish Federal Reserve risks a “Hawkish Hiccup”, especially between now and the end of Jerome Powell’s tenure in May.

Risks are consistently flagged in our team’s discussions, including fiscal imbalances, liquidity rollovers, asset bubbles, and geopolitical escalations, which could amplify volatility and trigger asset and currency adjustments. Action points, from our six lens approach to understanding the current environment and plotting probable forward pathways for asset markets, converge on overweighting equities in developed and South African markets, underweighting global bonds, and selectively engaging in commodity trades (bearing in mind how much commodity exposure is inherent in domestic equity holdings). At the same time, we advocate for active hedging through the use of options strategies in multiple asset classes and sentiment-based adjustments of our positioning. Being active will be key in 2026 as we think correlations will be higher than normal, so relying only on diversification, or traditional diversification, could be naive. While uncertainty is high (it always is), there are so many macro forces at play that, despite a challenging investment landscape in 2026, we believe it will present divergent opportunities and a fertile, and hence lucrative opportunity set, that we intend harvesting.

We have some concerns about the speed and pathways of further rate cuts, especially as market expectations have adjusted lower, prompting us to remove our New Regime scenario. This, broadly stated, was for rate cuts irrespective of inflation, which would support all assets, especially equities. This is now well priced in by the markets. While we acknowledge it is still in play, we see some risks from shifting expectations, similar to early2024, when a reduction in the pace of the lower rate path caused markets (not just equities) to adjust. To capture this risk, we have included a new scenario in our tactical work: “Hawkish Hiccup”. It suggests not just a central bank rhetoric shift but also growth, earnings proving to be hotter than we currently expect, job losses not as high as we expect and tariff impacts finally materialising. This is especially important as fiscal support widens around the world.

There are nuances in our view of the persistence of inflation, a key consideration impacting the direction, pathway and velocity of interest rates around the world. The synchronised global rate cycle is historic, and has been replaced not only by a varying pace in interest rate cuts between regions and countries, but, unusually, by the upward trajectory of rates in Japan relative to the rest of the world. We agree with the markets in expecting lower interest rates in the US and the potential ending of rate cutting cycles (we have stated that we think the cycle could be shallower than normal in the medium term) in some emerging markets and even in Europe and Australasia. In SA, rates are restrictive. While the agreed targeted inflation rate of 3% creates credibility for the South African Reserve Bank (SARB), it challenges business and consumer confidence, despite some small green shoots in policy and growth. SA’s terms of trade have never been better and are highly supportive of a stronger rand.

Global growth has proven exceptionally resilient through the cycle. Markets were not impacted by lower levels of growth. They were held upby liquidity from fiscal support which remained in the system after Covid. Our economics team is constructive on growth but is slightly less constructive than consensus. Europe has achieved stability (in inflation anyway, growth could be better). China maintains a policy floor, not arresting deflation but managing it, and US consumers are resilient, despite high living costs and housing pressures. Lower rates around the world reduce debt servicing costs, but fiscal burdens in economies like the US, France and Italy are offset by potential pump-priming in defence and infrastructure.

In the US, our economics team is concerned about the warning signs in soft data, which looks “patchy”. Data releases have been delayed due to government shutdowns, making it difficult to have a confident view in the short run. This difficulty is compounded by an economic trajectory impacted by the prevailing winds of fiscal and trade policy, immigration flows, AI capex, AI deployment and increasing geopolitical developments. In the short run we think our other tactical lenses provide clues. Some market signals look surprisingly “early cycle” for the US, but hopefully the variability of views within the team shows how open-minded we are to a range of economic outcomes. The soft data is concerning, and our economics team is worried that, beyond AI, the vibrancy of the US economy is being dampened. This is sowing some seeds of longer-term concerns to go with a long list of well-known issues that must be tackled to create sustainable long-term success.

Regarding policy, in our tactical horizon we think mid-terms in the US will increasingly impact Trump’s temperament and decision-making. His popularity is waning and concerns about a K-shaped economy are growing. We expect more policy support in the form of tax cuts and deregulation. This is where inflation will create some issues, not just for Trump but for policy makers. We were surprised that the expected tariff-induced inflation did not really materialise, and are watching for a shift in behaviour toward inflation expectations. Most importantly for our economics team, the decision and behaviour of the new Fed chair, who will probably be Kevin Hassett, will be one of the keys to understanding US policy in 2026 and also the dollar, bond markets and the cost of capital.

The behaviour of global central banks, which have cut interest rates while inflation is above inflation targets (most obviously by the Fed), was captured by our New Regime scenario in the last few years. We have used that scenario since the end of 2021, but now that the Fed has openly focused on unemployment, we think the market may start to react differently by making inflation secondary. We think that the Fed will now keep its focus on employment and job data. We believe it is now alive to what likely lies ahead with AI adoption - to their credit, Trump and Bessent have seen this coming and understand the need to get rates down, which also results in a lower interest cost on the very heavy debt burden.

The Fed must try to cushion against unemployment. However, with the One Big Beautiful Bill in effect, consensus economic growth picking up and migration impacts still making workers scarce, there is a risk that inflation will start to trend higher and even run away from the Fed. While we used to think that “New Regime” behaviour of cutting rates amid high inflation was a good outcome for markets, the markets have shifted to a similar view over the past few months. Given consensus thinking on lower rates, a consensus view we share, we are concerned that a shift in the narrative could turn the market environment a little less benign. This would harm bonds and potentially spill over into equities, challenging the bullish narrative we hold as a base case.

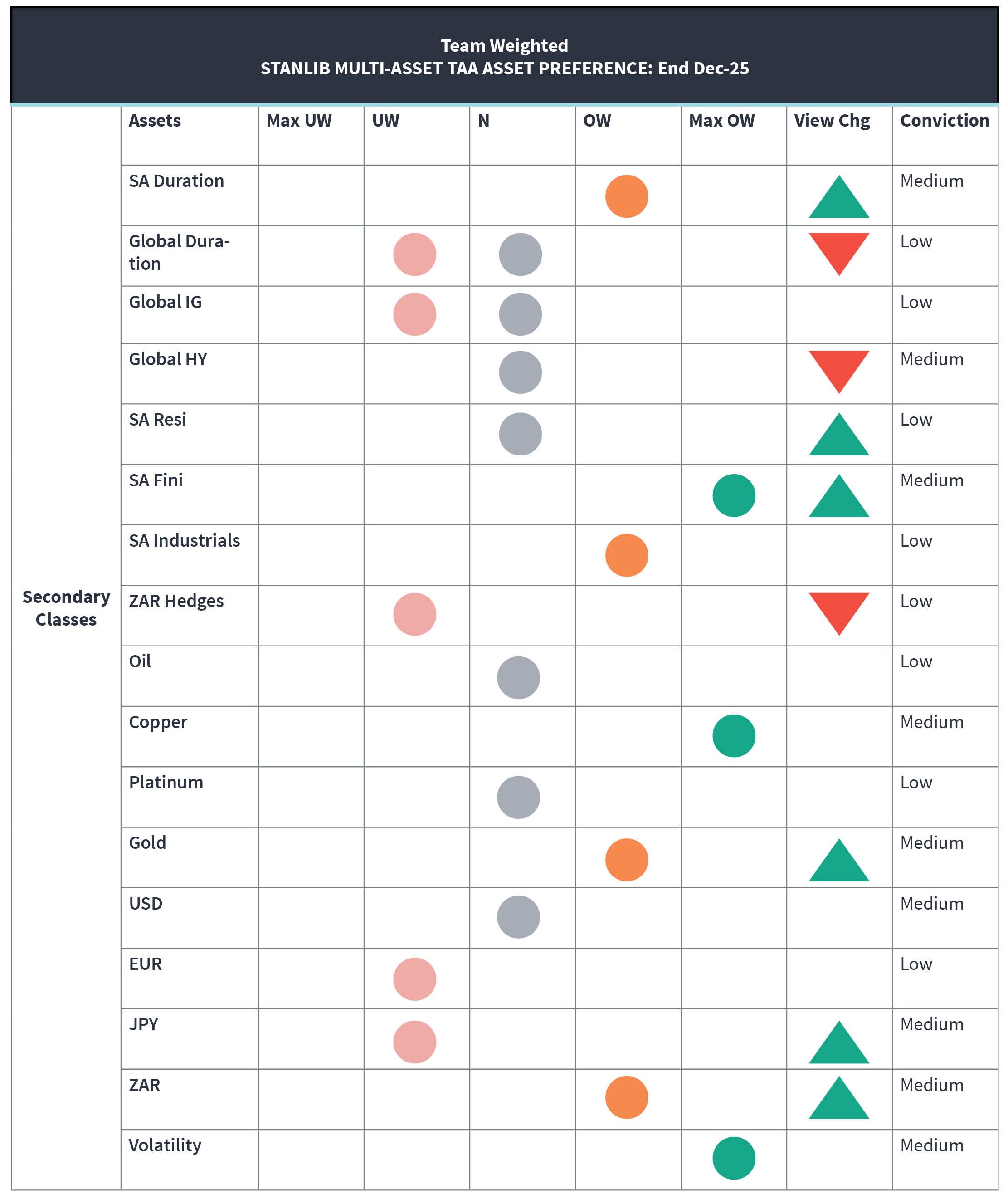

While supportive policy was largely limited to the US, in 2026Japan, China and Europe will begin to deploy their own fiscally supportive policies. This pathway from our New Regime scenario has now given way to“ Hawkish Hiccup”. While the scenario is not our highest probability for markets, it is not a tail risk. As a result, we question bond and rate paths more aggressively, which makes us reluctant to own many DM bonds. Some DM sovereign bonds are almost being seen as “return-free risk”. We continue to push for aggressive underweights in fixed income (how aggressive depends on the specific market), but the message is clear: we want to be underweight bonds.

Positively, SA has enjoyed an epic bond rally in 2025, and while we think there is potentially a little more juice left, it will be as lower move lower in yields. We think the SARB, while having room to cut, will be slow to act as it will continue to anchor inflation expectations at 3%. While there is likely to be an interest rate cut or two in our tactical time horizon, we think the risks to global rates limits the appeal of South African bonds. Pricing suggests duration, carry and roll down are likely to be higher drivers of fixed income returns than movements in short rates from an interest rate cut. We are therefore more focused on curve trades than increasing our weighting in domestic bonds. We believe domestic bonds are better than domestic cash, and are certainly better than broad global sovereign bonds, but they are no longer the dripping roast they were in the past few years. In the longer run, they remain interesting.

The economic outlook is one of balanced growth potential, tempered by uncertainties, with consensus on global growth possibly repeating2025's positive surprises but facing risks of dipping below trend. The TAA Framework details this, noting fiscal spending as stimulatory in the US, with most legislated cuts delayed until after 2026 mid-terms, and markets expecting Fed easing as a major swing factor. Questions arise about the Fed's cutting path, given above-trend growth and inflation, with potential hawkish risks from a new chair or shifts below neutral rates giving rise to credibility questions and inflation concerns.

Our Liquidity lens emphasises long-term vs. short-term perspectives. Liquidity has bounced but risks roll over as China and the Eurozone show peak short-term levels. Central bank actions are critical, with risks from inaction leading to market accidents.

US Treasury Secretary Scott Bessent, with his understanding of macro market behaviour, has been controlling fixed income pressures – which are being felt around the world - by managing the US bond curve. The issuances of bills at the short end of the bond curve are at much higher amounts than issuances at the longer end of the bond curve. This has meant that the US 30-year bond has been well behaved, despite the narrative of long end yields backing up, which is very much the case in Japanese government bonds, a predictable but still worrying development over the last few years.

While curve control is alive in the US (and elsewhere), the end of quantitative tightening occurred on 1 December 2025 (QT is in itself a form of tightening financial conditions). It has been in place since 2022. That event was a big signal for us, especially viewed through our liquidity lens. The Fed cut rates by 0.25% on Wednesday 10 December and announced that it would be purchasing $40 billion a month of T-Bills as part of “reserve management asset purchases”. Many people might argue the technicalities but to us this is a form of QE, especially combined with Bessent curve control. This has happened sooner than we thought, and we expect it will happen soon in Japan. In the short run, it is positive for equity markets, but lays another brick in the wall of worry about the path of inflation and hence for bonds (at some stage).

Liquidity is a major tailwind. Most countries we monitor are displaying positive liquidity metrics in the signals we track, with emerging markets like Brazil, Turkey, and SA showing improvements. SA’s metrics specifically are strengthening, aligning with our investment framework around “change” and “reform-driven developments” observable in many pockets of asset markets, not always positively.

Our scenarios show that bearish probabilities have faded but our new "Hawkish Hiccup" amber scenario is weighty. Challenges are a positive liquidity backdrop by design, implying policy and market friction, with more downside potentially ahead. This aligns with broad concerns about risks punctuating our discussions, and our soft vs. hard landing debates. Easing reduces debt servicing costs, but fiscal burdens in core economies like France and Italy are offset by potential pump-priming in defence and infrastructure. Conflicting news and policy will remain with us in 2026.

Key Themes and Views

Early Cycle

A key overlapping theme is the "early cycle" concept in global markets. We note that we are in a phase when policy support—fiscal stimulus and monetary easing—creates mini-cycles in credit, earnings, volatility and behaviour that are decoupled from traditional GDP fluctuations. Our observations are that current policy interventions are stronger than in post-Global Financial Crisis periods and will allow for sustained corporate activity such as mergers and acquisitions, initial public offerings, and capital expenditure cycles. Tariffs are accepted as part of the current regime but are now in the consensus thinking, moving into the base and counteracting positives that are emerging. Importantly, we believe household and corporate wealth is very high, enhancing re-leveraging expectations and ample liquidity, which facilitates carry trades amid another temporary dollar dip. The early cycle hypothesis translates into practical positioning, such as overweighting developed market equities and South African Inc stocks, underscoring the consensus that equities represent the "least-worst" risk asset in an environment in which bonds are less attractive due to fiscal concerns and elevated volatility.

Artificial Intelligence

The transformative impact of AI is a recurring theme. Our momentum signals show strong earnings growth in Asia led by AI cycles, and continued high conviction in AI as a structural long-term theme, recommending broad thematic exposure over single-stock picks due to winner uncertainty. This theme is not only about semiconductors or technology. There are many ways to play it, especially as our thinking and countercyclical signals – captured to varying degrees in our volatility and sentiment lenses - caution on short-term volatility or corrections, but the overall view is positive.

We think2026 will start showing AI impacting profits and jobs. How much it will impact consumption in the US is a key theme to watch, as we could potentially see the K-Shaped phenomenon of the US economy start to be felt by the middle class.

Diversification and flexibility will be key. We always seek diversification in allocations across assets, factors, regions and sectors. To reduce concentration risks, we think active management will be very valuable as it enables thinking about where the diversifying assets are and hedging these fast-moving markets and changing characteristics of assets. When a supposedly “defensive asset” like gold has higher volatility than a traditional “high-risk” asset like equities, theoretical thinking has to be revisited. In SA, if the gold rice reverses, equities, bonds and currency are likely to feel the effects at the same time.

Dollar weakness – for now

Emerging markets are positioned as growth engines, contributing 40% of global GDP and 70% of real growth but only 11% of major index weights. Drivers include AI, commodities, high-tech manufacturing, infrastructure, and consumer demand. Equity valuations are relatively attractive at a 32% discount to developed markets and 20% earnings growth forecast for2026, led by Asian AI. But this does not make emerging market indices an automatic buy, despite the improving breadth in our momentum signals.

Regions like Emerging Asia, Emerging Europe and Latin America historically benefit from dollar declines and robust capital flows. In this cycle, cyclical growth is not as clear a signal as it was before, and the softer dollar is lower for different reasons than robust growth elsewhere.

The easing cycles are much further along in most Emerging Markets. Stable credit ratings and decent central bank policies have resulted in reduced volatility and in some cases lower volatility in Emerging Market bonds than even in some developed markets.

As highlighted in our “Hawkish Hiccup” scenario, we think there is a risk that the global easing cycle is nearing its end, limiting yield declines from here. South African 10-year yields are higher than in many other places around the world. They are offering an 8.6% yield, with the SARB expected to cut by 25 basis points then hold. The rand is still undervalued relative to its carry, our central bank is growing in credibility, but we need growth to offset some of the fiscal concerns that remain. Fiscal and global volatility could raise our bond yields again but overall emerging market bonds are selectively overweighted, especially those of SA, Brazil, and Mexico. This reflects yields and fundamentals, which are dependent on liquidity and our view on the dollar and other developed market currency paths.

In SA, we have mentioned bonds are fair to attractive. Equities look reasonable from a valuation perspective relative to their own history and are a little more appealing than SA bonds after the strong fixed income rally. We think much good news has been priced in, and relative value curve management will drive fixed income returns in the short run, as well as getting global bond views and anchors correct.

Global equities continue to appeal to us. Not for the first time, we note US small- and mid-caps are undervalued compared to large-caps, aided by interest rate easing and lessening of tariff exposure as the economy moves into “base effect” mode. However, the AI theme is big, and we think earnings, margins and growth will remain most prevalent in the S&P 500, and tech/AI. Concentration is high in the S&P 500: almost 40% of the S&P 500is concentrated in the top 10 largest names but that does not mean the AI theme is over. We expect AI will have a positive effect on equities in 2026.

In emerging market equities, SA looks relatively attractive. Although we like gold again, having moved back to neutral last quarter from overweight, we are concerned about the concentration of precious metals in our equity markets. The gold price impacts our fixed income and currency markets and there is a huge positive from stronger gold but a hiccup could change a huge portion of our portfolios at the same time. So while we like gold as an asset, from a portfolio construction perspective, it is not one we are explicitly adding to portfolios. We already inherit exposure from our passive equity and index derivative positions, SA bond holdings and some of our currency positions. In domestic equities, sector attractiveness includes South African banks and insurers, which are compelling as valuations are lagging bond repricing. Momentum varies by sub-sectors like gold, PGMs, and diversified mining, complicating diversification. Listed Property is quite attractive but liquidity is constrained.

China's outlook is nuanced: with growth stabilising at 4-5%,the Chinese are maintaining a policy floor. The market hopes for stimulus that will lead to a rebound against headwinds like overcapacity, deflation, and trade tensions with the US. Liquidity is positive but at risk of fading and we continue to worry about consumers’ reluctance to deploy capital. We think we understand why, and that keeps us watching rather than wading into China outside selected opportunities. We don’t believe that fiscal support, even if it comes, will persuade consumers out of defensive mode.

Currency views overlap on weaker dollar consensus, supporting Emerging Market foreign exchange and the rand. We remain long the rand for carry against yen and a non-consensus position that helped in 2025. We note the SA currency-bond correlations and are wary of stacking risks.

Core Risks

Inflation resurgence from tariffs, services, or fiscal policy is a core risk, constraining cuts, and perhaps even leading to hikes in certain parts of the world, which would hit bonds hardest. Geopolitical uncertainties abound, with elections, gridlock and tensions in Ukraine/Russia/Middle East/the South China Sea. This will drive volatility, with fiscal expansion raising debt concerns and risk premiums. Recession risks, labour weakness from AI, China deflation, policy errors in any number of areas, de-dollarisation and its speed and sector vulnerabilities arising from any of this non-exhaustive list of risks could trigger market gyrations.

Current Working Scenario Summaries

Multi-Asset Team Current Asset Preferences:

Conclusion

In 2026, adaptability and discernment will be the hallmarks of successful investing. The environment is dynamic - shaped by shifting policies, evolving risks, and transformative technologies. For us, the challenge is to embrace change with agility and conviction when we have it. As we remain open to new opportunities, vigilant to emerging risks, and committed to active management, we believe 2026 will present plenty of opportunities for delivering returns.