A long war or a short war? STANLIB fixed income team positions for both outcomes

The outbreak of the US/Iran war has rattled global economies and risk assets, triggering a sharp reaction in the prices of oil, gold, shares, bonds and currencies. If the war is prolonged, steeply higher fuel prices will create inflationary pressures around the world, which could compel central banks to hike interest rates.

Since war broke out, the South African bond market has repriced by about 120 bps. Importantly, the short end of the curve has moved up materially. Up to mid-March, foreign investors were net sellers of R29bn of SA bonds, although in the year to date they remain net buyers of about R22bn. The biggest foreign sellers have been hedge funds taking advantage of volatility, while long-only portfolio managers have been buying into weakness or waiting to identify pockets of value.

The Fixed Income team is drawing on its experience of previous oil shocks to assess how central banks will react to events. The team’s scenario approach, along with its fair value model, enables it to “cut out the noise” and consider only what will affect bond prices, inflation, growth and central bank responses.

SA’s interest rate outlook has changed.

SA’s headline inflation rate fell to 3% in early February from almost 8% in 2022. In 2022, the increase reflected the Russian invasion of Ukraine, which drove the price of oil up from $80/barrel to $127/barrel, following a period of post-Covid stimulus by central banks. In response to higher inflation, the South African Reserve Bank (SARB) hiked interest rates from 3.5% by 75 bps increments to a peak of 8%.

This time is likely to be different because inflation is being driven by supply, not demand, in an environment where SA’s growth rate is low and core inflation has been muted for some time. For the SARB, the neutral real rate (repo rate less inflation four quarters ahead) is 2.7% – a level that would neither constrain growth nor feed inflation. Currently, the real rate is 4%, which is restrictive, and given SA's low growth rate, interest rates should be accommodative.

Before the war, forward rate agreements (FRAs) were indicating two rate cuts by the SARB this year, based on economic fundamentals. Now FRAs are pricing in three rate hikes by the SARB in 2026 as inflation, driven by oil prices, is expected to rise above its 3% target.

A short war would not alter SA’s economic fundamentals. GDP growth has averaged 0.7% a year over the past 10 years, well below the government's 3% ambition, but was starting to move up. In 2025 the SA economy grew 1.1%, and we expected it would rise to 1.5-1.6% in 2026 due to reforms under way. Now this year’s growth rate is forecast to be similar to 2025's.

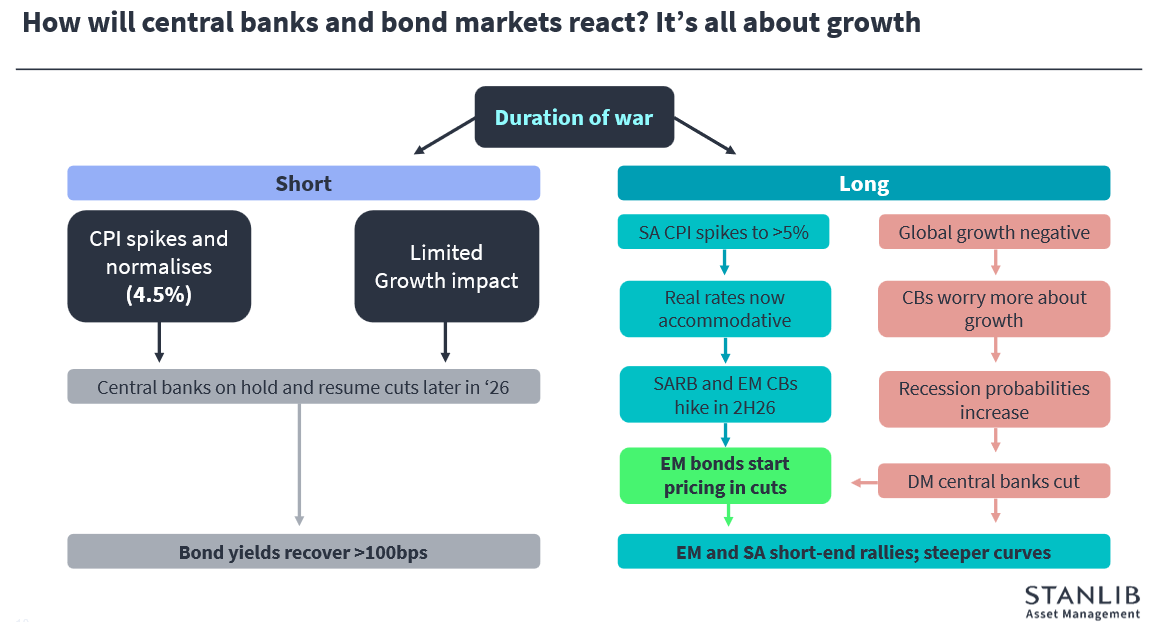

Two possible scenarios

The team is considering two different scenarios: a short war (lasting about a month) or a longer war (until end-2026).

It is worth remembering that the increase in the oil price has had an immediate effect on US consumers, who are already struggling because of tariff hikes. The US economy shed 92 000 jobs in February 2026. The war is politically unwelcome, especially ahead of a midterm election.

If the war is short:

- SA’s April inflation rate will spike above 4% due to fuel price increases, but it would be a short-term event with no material impact on growth.

- Global central banks will hold rates until the end of 2026 and then resume interest rate cuts.

- The STANLIB Fixed Income team expects one or two interest rate cuts in SA in the second half of the year. In that event, bond yields should recover by at least 100 bps.

If the war drags on until year-end:

- SA’s inflation rate could spike to 5% or more.

- At 5% inflation, given the SARB’s neutral real rate of 2.7%, domestic interest rates should be 7.7% - from 6.7% at present. That would indicate the SARB and other emerging market central banks would have to hike rates to control inflation expectations.

- In this scenario, global economic growth becomes a concern. Higher oil prices reduce consumers’ purchasing power and, if accompanied by another shock (e.g., a political event), the impact on growth is even greater.

- In an extended war scenario, recession probabilities will increase and developed market central banks will cut rates to shield their economies, followed in due course by emerging market central banks.

- This would cause the short end of the bond curve to rally and outperform the longer end, which would reflect concern about greater government spending.

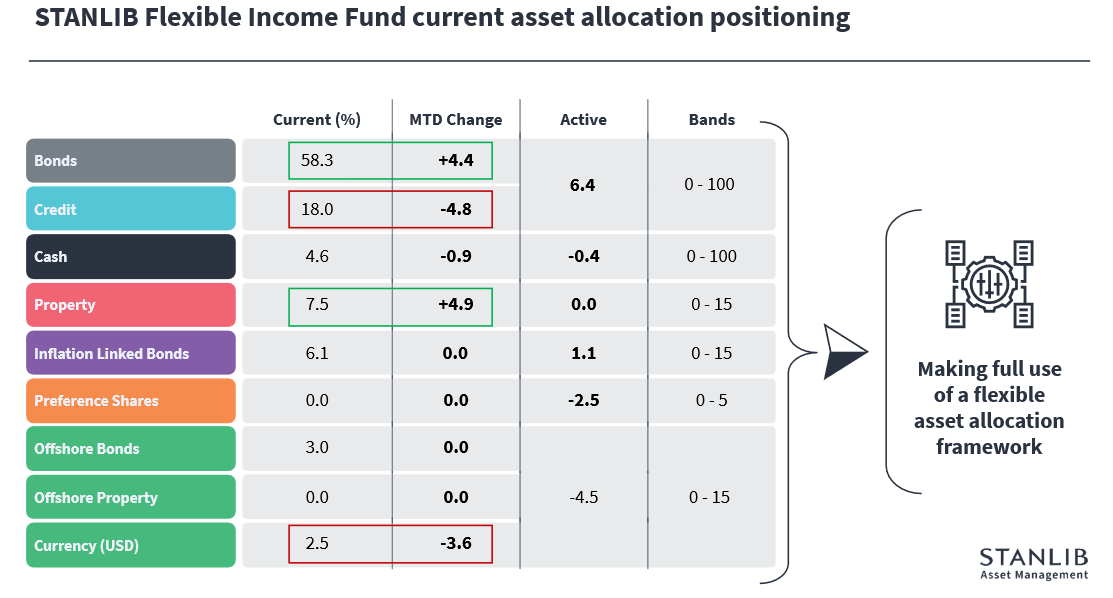

Repositioning the STANLIB Flexible Income Fund

The STANLIB Flexible Income Fund is actively managed and constantly looking at opportunities to take on risk. Unlike other domestic fixed-income funds, its mandate allows it to invest up to 10% in offshore bonds. These generally deliver far lower yields than SA bonds, so their main function in the portfolio, together with the currency, is to provide a currency hedge, which pays off when the rand sells off.

Before the war broke out, fundamentals appeared strongly positive for domestic bonds due to momentum on inflation and growth, but even then the team considered a Middle East war and local politics as potential risks.

- The managers took protective measures in the STANLIB Flexible Income Fund, building up dollar holdings to 7.1% of the portfolio when the rand was strong.

- After the sell-off in the rand and bonds, the team took profits, taking the dollar holdings back to 2.5% of the portfolio, and bought back into short-dated bonds at lower levels, as well as domestic property.

- Duration remained at about three years, but the portfolio is now heavily overweight in bonds. Fair value for the SA 10-year bond is estimated at 7.5%, and the team is comfortable that the latest developments do not undermine the National Treasury’s budget projections, which were conservative. However, the picture will change if the war is protracted.

- The portfolio has remained overweight inflation-linked bonds, which would benefit if inflation spiked.

We remain nimble: if the war escalates and affects oil infrastructure, the portfolio can be adjusted within a day – as the team did during Covid.

Repositioning the STANLIB Income Fund

- Before the war broke out, the STANLIB Income Fund’s yield was projected to be about 8% or less for 2026, given three interest rate cuts by the SARB this year. The yield is now expected to move higher and end the year at 8.76% as the market starts to anticipate rate hikes.

We are not concerned about instability in private credit markets, as the STANLIB Income Fund holds high-quality credit assets, with an average credit rating of AA-.

The STANLIB Income Fund is a “sleep at night” fund, which targets a return of 200 bps above a money market fund. It takes duration positions from time to time to enhance capital growth, and there could be an opportunity to increase duration if the war ends soon. Investors in this fund should be looking at longer-term moves, not daily pricing.

Confidence in sustained returns

The flagship STANLIB Flexible Income Fund attracted over R2bn of net inflows in 2025.

Up to the end of February, the STANLIB Flexible Income Fund has delivered a 12.6% gross return over one year, 12.3% p.a. over three years and 10.7% p.a. over five years.

The goal is to deliver 1-2% of alpha over a rolling three-year period, which the fund has consistently surpassed. Although March’s returns will be lower, the team is confident of achieving another year of 3% alpha or more.

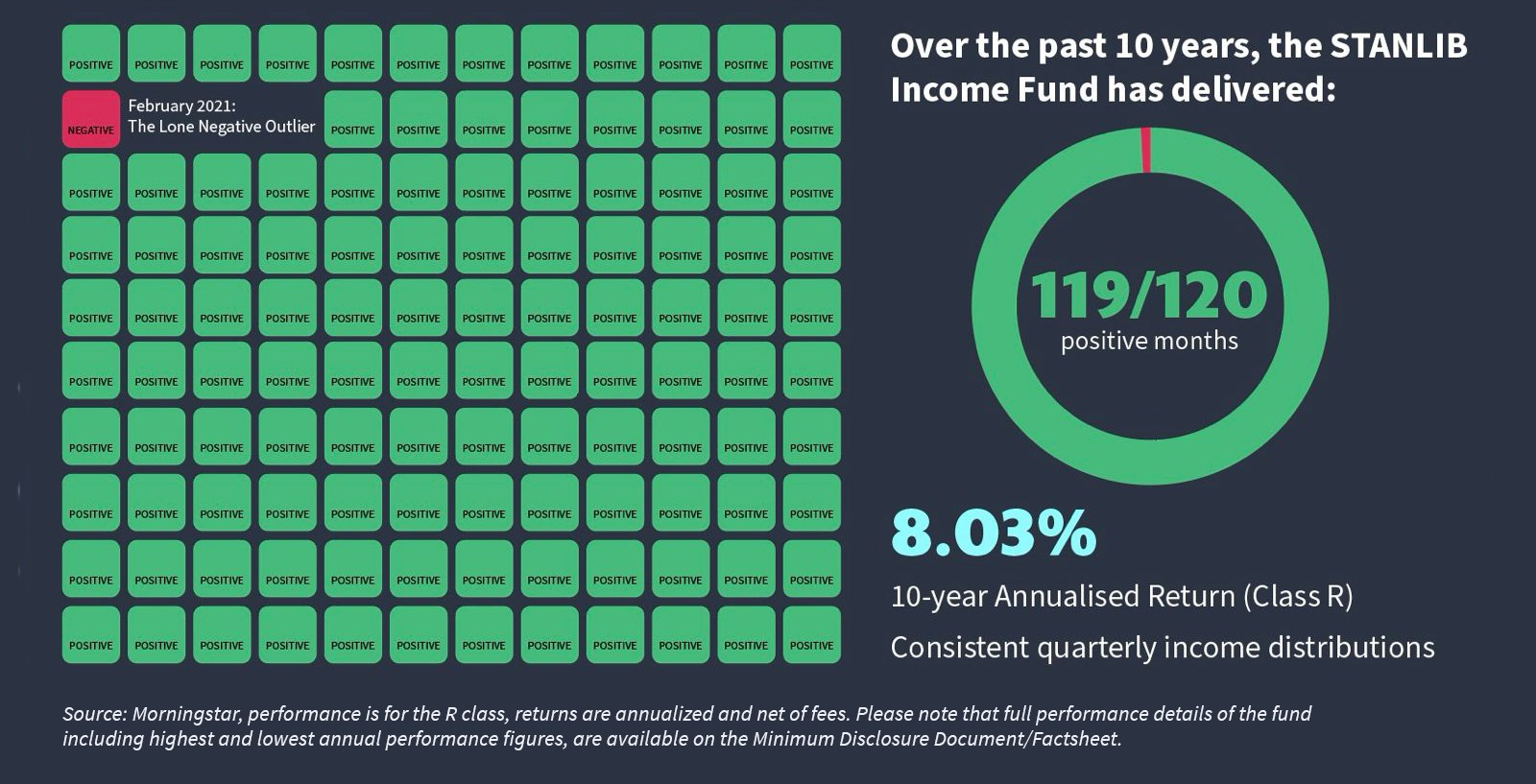

The R65bn STANLIB Income Fund has delivered only one month of negative returns in the past ten years. The chart below displays the monthly STANLIB Income Fund (Class R) returns over the last decade:

To find out more about the STANLIB Flexible Income Fund, speak to your STANLIB Asset Management Investment Specialist or click here.