The rules of the game are changing – putting increased pressure on the investor

The goal of investing during retirement is simple: to maintain a real income for the rest of your life. By excluding growth assets from your portfolio, and drawing down too much income, you are setting yourself up for failure.

Various changes to the South African retirement landscape over the years have, despite good intentions, actually made it harder for financial advisers to ensure their retired clients do not outlive their capital. For example, the move from defined benefit to defined contribution funds means that investors can now control 100% of their retirement funds – but they also take on 100% of the investment risk and 100% of the longevity risk. Despite some positive changes, SA’s retirement tax regime remains less favourable than in many other countries, such as Australia. Amendments to Regulation 28 over the years have permitted a wider range of assets for retirement capital, including more offshore holdings, which has been a very positive development. However, this needs to be managed carefully as it also results in a wider dispersion of returns.

More “noise” in the information age generates market volatility, which in turn prompts the urge to act in investors, which can result in investment mistakes like selling after a crash before the subsequent market recovery.

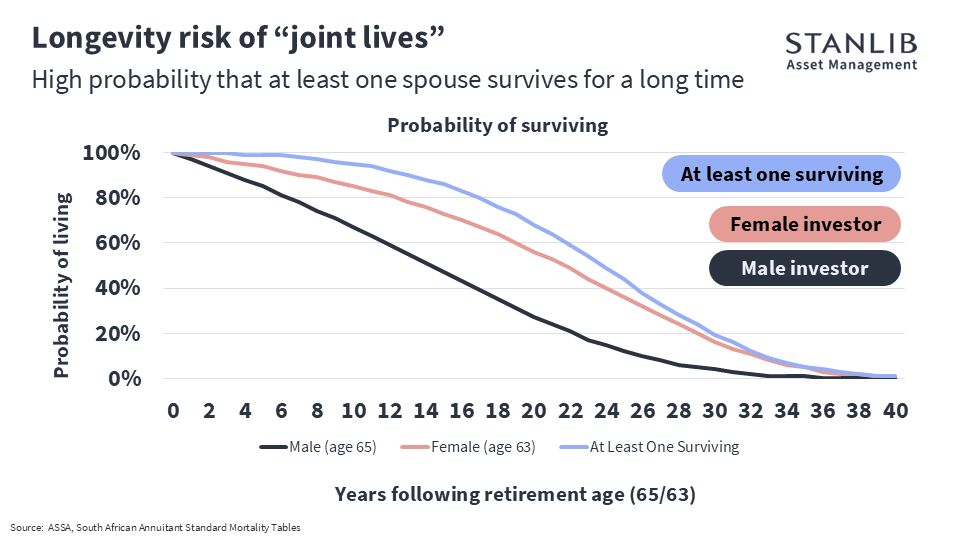

It is also well-known that both men and women are living longer. Retirement capital has to last, not just for the lifespan of one partner, but until the last surviving spouse dies. That means at least 30 years after they retire at 63 or 65.

What are the options?

The options available to most retirees to preserve capital as long as possible and generate a real income from it are living and guaranteed annuities. Guaranteed annuities provide a longevity guarantee that living annuities do not, but the flexibility is traditionally lower.

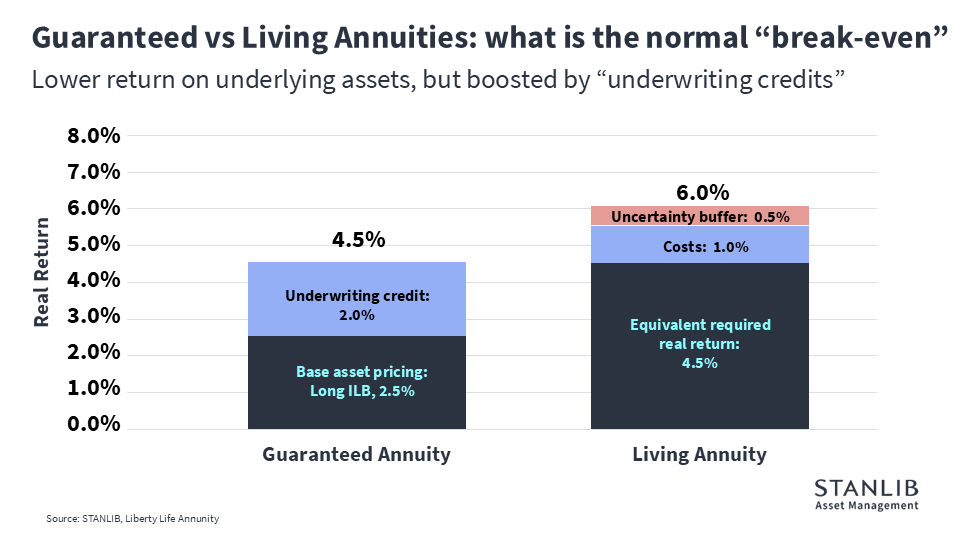

The pricing of atypical guaranteed annuity is based on long-term inflation-linked bonds, which in SA generally deliver a real return of about 2.5% p.a. That return is enhanced by the underwriting credit (the cross-subsidisation of longer-lived members in the scheme by those who die younger) of ±2% p.a. In total, this delivers a typical starting income yield of about 4.5% of retirement capital, which increases in line with inflation, throughout the annuitant’s lifespan. Currently, long-term inflation-linked bonds are offering better returns than 2.5%p.a. real, at 4.1% p.a. currently. With the underwriting credit, the starting income yield from a guaranteed annuity becomes 6.1% a year, at current yields.

To be more attractive than a guaranteed annuity, a living annuity has to at least outperform 4.5% plus a margin of say 1% for costs, together with an uncertainty buffer of about 0.5%, which means it has to deliver a total of 6% (or 7.6%, using current ILB yields).

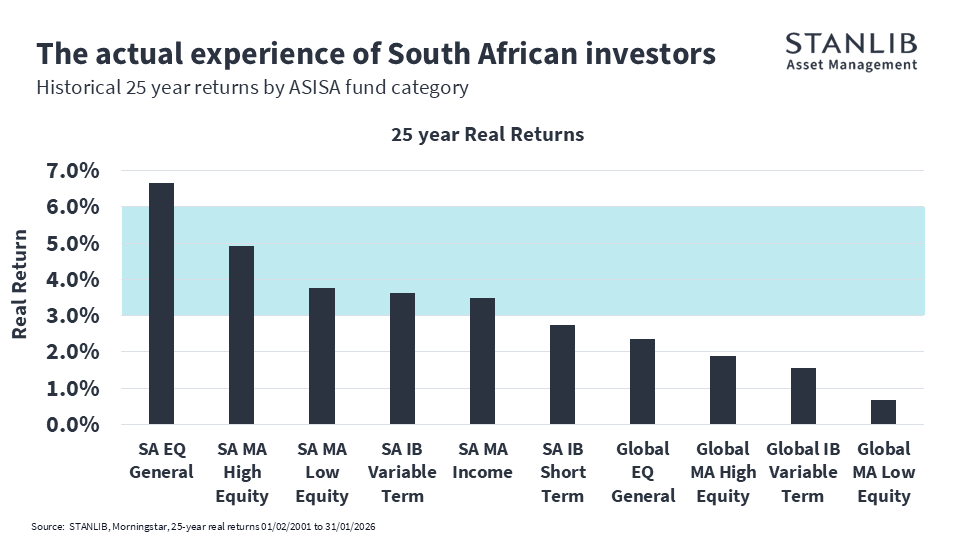

Analysing the historical real performance of South African assets that would typically be included in a living annuity (based on ASISA categories and a 25-yearhorizon) shows that the only category that has outperformed 6% is South African Equity General. Low equity multi-asset funds have delivered only 1-2% a year on average over the past 25 years.

Living Annuity scenario modelling

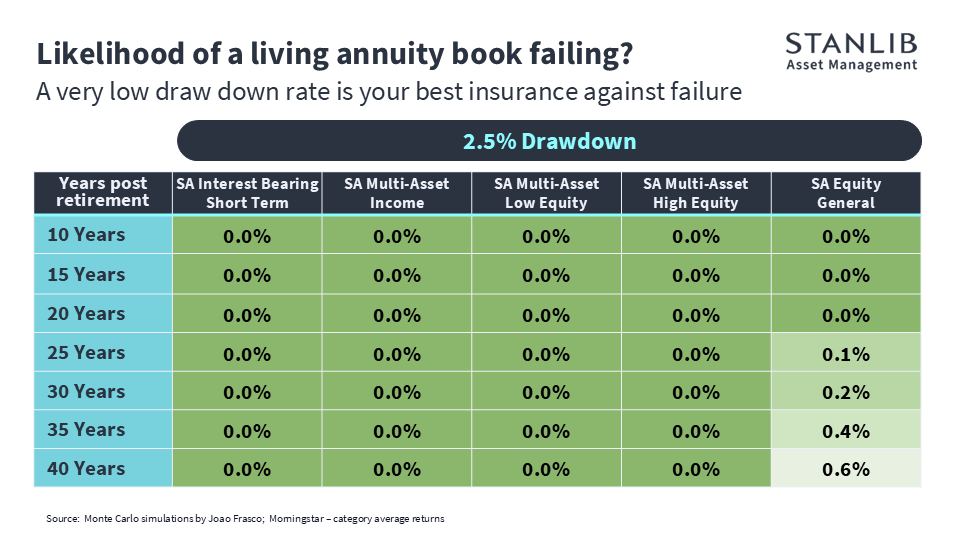

All financial advisers have personal biases when it comes to choosing living annuity constituents. To avoid bias, the STANLIB Asset Management team performed an exercise, using Monte Carlo* modelling, to find out how living annuity holders would have fared if they were holding one of the typical South African funds over the past 25 years, using actual investment returns and assuming a sample size of 10 000. This simply means that if you start with a group of 10 000 investors all retiring, and invested into each of these funds, how many of them would run out of money before each of the future points intime? The range of funds includes the average fund from the SA Interest-bearing Short Term, SA Multi-Asset Income, SA Multi-Asset Low Equity and SA Multi-Asset High Equity fund categories.

We initially modelled using a 2.5% annual drawdown rate. The results showed that the likelihood of the retiree with a living annuity based on one of those categories running out of money after 40 years was zero, or close to zero. However, there was a small chance of running out of money if the living annuity was invested in the SA Equity General category, because of the volatility of equity returns. A 2.5% drawdown rate is clearly a safe level.

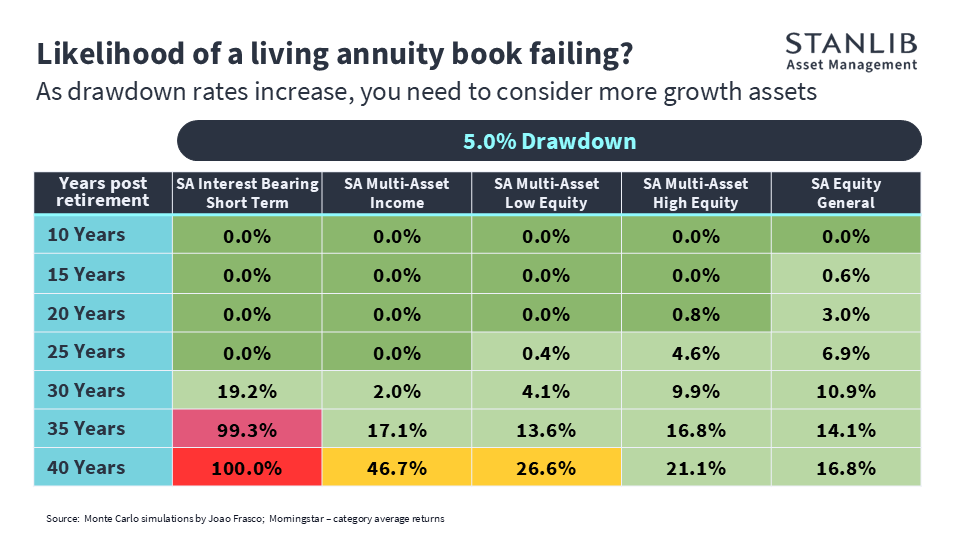

Modelling with a drawdown rate of 5% showed the category most likely to result in the retiree running out of money is SA Interest-bearing Short Term, because it is not delivering a high enough return to last 40 years.

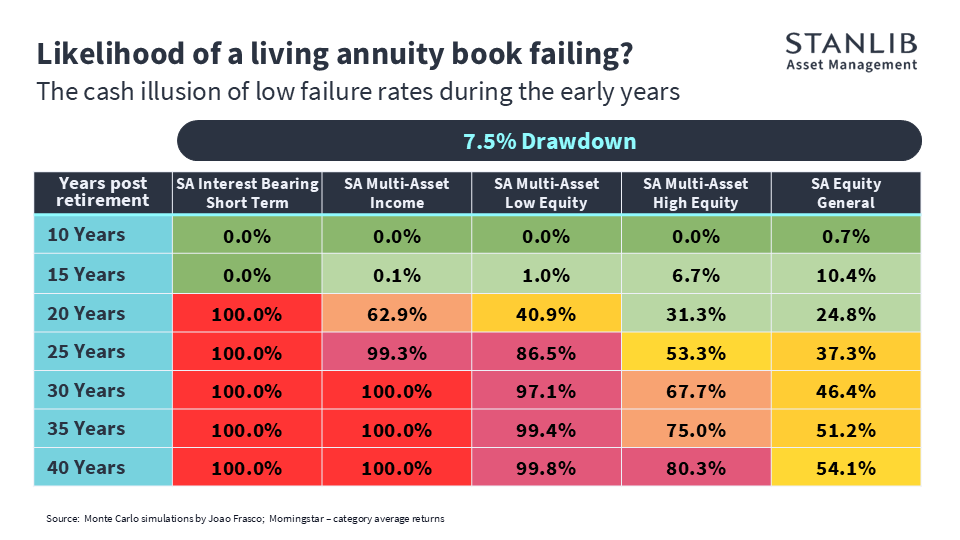

Using a 7.5% drawdown rate, which an ASISA study shows is the average drawdown rate in SA, shows material failure rates, whatever category is chosen.

Most retirees don’t realise the longer-term implications of drawing too much. The first 10 years after retirement is the “honeymoon period”, when living annuities don’t fail, largely irrespective of the investment returns and drawdown rates. At higher drawdown rates, they can start to fail after about 20-25 years.

Planning for success

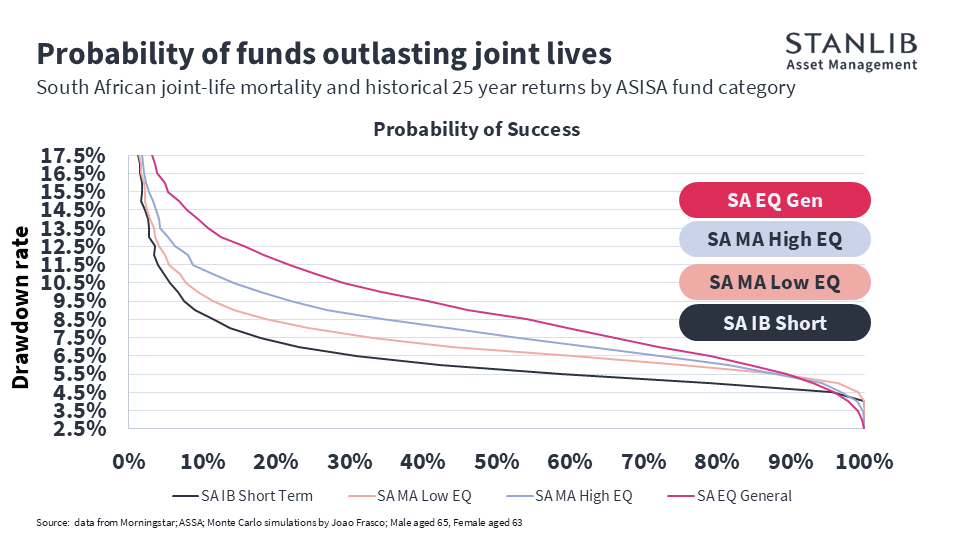

While the above scenarios only look at the investment side of things, in real life there is the risk of longevity, i.e. living longer than your money lasts. A successful outcome is therefore defined as the scenario where the retirement capital pot is not depleted by the time the last surviving spouse dies. As the drawdown rate decreases, the chances of success increase. At a lower drawdown rate, even a lower equity portfolio will be more successful than one with no equity.

But the lesson is not that advisers should put all their clients’ money into equity funds. The lesson is that in a living annuity, it is important to ensure there are sufficient growth assets to generate the real returns to ensure capital keeps up with inflation.

Many people think it is not necessary to choose between a guaranteed or living annuity. They typically think a retiree should invest in a living annuity at retirement and shift to a guaranteed annuity 10-15 years later. Various models have shown that is not a good idea.

If a client does not select a guaranteed annuity at retirement at 65, but delays doing so for five years, they will need an additional 3% growth in the portfolio (8% growth, not 5%). If they delay the move for 15 years, they need an additional 4% growth in the portfolio (9% a year). The reason is that a surviving 80-year-old retiree who buys a guaranteed annuity joins the pool of other 80-year-olds and does not benefit from the cross-subsidies contributions of those who died younger.

The key take-out is that the “price” of both guaranteed annuities and living annuities isn’t static. They depend on the valuation of the underlying assets at the time you invest. One therefore needs to consider the current asset valuations in conjunction with all the other variables, and act accordingly. It is also not an “either or” decision between both guaranteed annuities and living annuities, but rather that both can be used in appropriate proportions to ensure the retirees’ income can last for their entire life.

In summary

Retirement planning needs to be for both spouses, not the main member. Putting low-risk assets into a living annuity (because you are risk-averse and don’t want to experience volatility) is “planning for failure”. The old practice of de-risking a retirement portfolio on retirement date to avoid market volatility actually means giving up growth assets when the investment pot is greatest.

The price of guaranteed and living annuities is not static, so financial advisers cannot use static models. They should watch the latest pricing before making a decision. Financial advisers and their clients should be aware that the sustainability of a living annuity is highly sensitive to drawdown rates which investors should therefore manage very carefully throughout their retirement. Finally, if advisers and their clients want to use a guaranteed annuity within their overall retirement portfolio, they should do so at the outset.

* A Monte Carlo simulation is a mathematical technique that models the probability of different outcomes in a process involving random variables. Instead of giving a single, fixed prediction, it uses random sampling to run thousands or millions of scenarios, revealing the full spectrum of possible results and how likely they are.