The retail sector perspectives on global trends

Neil Robson

Head of Global Equities at

Columbia Threadneedle Investments

As consumers are shifting to online shopping experiences, landlords are agreeing to rental concessions. Our global equities portfolio manager shares some interesting perspectives.

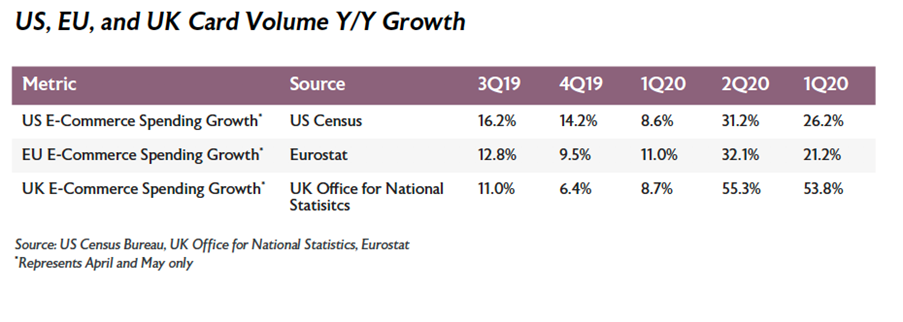

A major acceleration in the long-term trend for e-commerce to gain share within retail sales overall has resulted from the COVID-19 crisis. At a time when our mobility has been constrained in an effort to lower infection rates. This has been a trend globally as can be seen in the credit card data for online spending in the table above, where in Q2 this year over year spending grew 31% in the US, 32% in Europe and an astounding 55% in the UK.

The figure below shows the jump in the penetration of online sales in the US from under 12% to over 16% (in the UK, this rose from 20% to well over 30%). This is a significant acceleration on the prior trend. There is cause for caution, as some of this change is due to the fall in overall retail sales (the denominator), rather than just the growth of e-commerce.

Of course, this penetration rate will drop once this crisis passes, the physical retail infrastructure reopens fully, and consumers’ confidence recovers. However, some changes will remain.

Analysis shows that it takes 60 days to form a new habit, and we have all lived for far longer under COVID-19, many in lockdown conditions. Almost everyone will have experimented with buying something new online, and some of those habits will stick, as the convenience and price point of e-commerce, or simply the habit, will influence our behaviour.

What will the important shifts be? For me, who had rarely ever shopped online, it was small items like guitar strings and vinyl records – and I don’t see myself going back. The big category in which the online businesses have been investing to break into is groceries, and for many, this crisis has been our first experience of buying our food and drink online – everything from toilet rolls and flour (apparently, we all tried to bake at home), to meal kits. I believe this spending pattern has started a permanent shift online.

Traditional retail formats have done their best to adapt, shifting to a multi-channel offering and investing in their online offering and fulfilment. For large businesses like Walmart, this is a continuation of strategy, and one they can afford, but for many small businesses, it is impossible to match the fulfilment capabilities of the giants like Amazon. To offer next-day or even later-inthe-day delivery takes enormous investment, and Amazon has not been a standing target. Amazon themselves have invested aggressively to further embed themselves in our habits, hiring some 175 000 new employees since the crisis started.

Physical retail seems stuck in a never-ending restructuring, ceding space to focus on prime/destination shopping centres, while focusing on a highly curated/high-end offering. Are we at the end of the shift online? No, perhaps it has just shown us a glimpse of the future. If the UK can get to over 30% of retail sales online, why not the US? If 30%, why not 50%? The implications for retail still look bleak – vacancy rates are likely to rise further, and we will see further bankruptcies in the sector.

One change that may become semi-permanent is the location of our consumption. At Columbia Threadneedle, we have been working from home for many months now – we are no longer buying our lunch at Pret or Marks & Spencer, and we are no longer shopping near St Paul’s.

While I am sure we will return to the office in time, I believe we will all work from home more frequently than in the past. If we all worked one day a week from home, I am sure there are many retail businesses local to our office that will struggle to adjust to a -20% drop in revenues. This is a further threat to the sustainability of our towns and cities, and as retail vacancy rates grow, the appeal of the physical retail experience declines.

Conversely, is there an opportunity for retail in our small towns and villages once their role as dormitory towns is partially reversed and office workers’ consumption shifts back to where they live?

Behind it all, a key trend has been the growth of ‘shopping with purpose’, as consumers of all ages become increasingly aware of the social and environmental implications of their consumption.

The existence of COVID-19 itself is cause for thought in this regard. The range of implications is extremely broad, from a shift towards a plant-based diet with benefits on climate change, to an aversion to fast fashion and the throwaway society.

I enclose a link to a piece written by my colleague Pauline Grange on the efforts of one company in our portfolio, Adidas, in this regard. It describes her visit to the company’s new flagship store in London, and clearly demonstrates their environmental intent in their changing product offering and using the store as a brand promoter. All of this sits in front of their massive investment in their direct to consumer online offering and suggests a dim future for footwear stores and sports shops. Click here to read article.

In the global equity portfolio, we have no exposure to traditional retail formats. Instead, we have investments in the two pre-eminent online retailers worldwide, Amazon and Alibaba. We also have exposure to brand businesses, like adidas, who have some exposure to physical retail. Finally, we should not forget that the rise of e-commerce cannot exist alone, and has profound implications for associated businesses like the payments industry and advertising, where we also hold significant investments.

This article appears in the Q4 November 2020 edition of our StandPoint publication. Click here to download a copy of the full publication.