Low interest rates and high government debt have become the norm

Kevin Lings

Chief Economist

Global GDP is on track to record an unprecedented decline in economic output during 2020 of around -4.4%.

‘Unconventional’ policy measures

Understandably, in early 2020, governments and central banks quickly came under enormous pressure to respond to the crisis. This included a substantial increase in government transfers to support businesses and the household sectors, but also an increased effort by central banks to provide further monetary policy relief.

While some central banks, like the South African Reserve Bank, had scope to cut interest rates further, most major central banks did not. With little or no scope to reduce interest rates any further, they were forced to expand their use of ‘unconventional’ policy measures, such as quantitative easing or yield curve control to provide financial market stability and sustain economic growth.

These policy initiatives manifested in a rapid expansion of both government and central bank balance sheets, especially within developed economies such as the United States, United Kingdom and Euro-area. In particular, most of the large central banks now own vast quantities of risky assets, including government bonds.

For example, by the beginning of October 2020, the United States Federal Reserve had accumulated a phenomenal $4.88 trillion in US government bonds. This, compared with less than $600 million prior to the 2008/2009 global financial market crisis. This perpetual accumulation of government bonds by the large central banks effectively allowed governments to run much larger-than-normal fiscal deficits, confident in the belief that their central banks would continue to accumulate a significant portion of any outstanding government debt.

Consequently, what started as a set of temporary but ‘unconventional’ monetary policy measures at the time of the global financial market crisis in 2008/2009, have now become a permanent component of central bank monetary policy.

From a central bank’s perspective, they would argue that they needed to introduce this unprecedented set of policy measures to prevent the global economy from collapsing into another depression. Furthermore, central banks have vowed to withdraw the extraordinary policy measures once the crisis is over. However, just like the quantitative easing enacted after the 2008/2009 global financial crisis, shutting off the liquidity tap could prove more challenging than opening it.

This signals that there has been a paradigm shift in the management of monetary policy

Most central banks can no longer afford to simply focus on only one primary policy objective, namely achieving their inflation target. Instead, they need to prioritise ongoing financial market stability, while at the same time stimulating economic growth. This change in the role of central banks runs the risk of severely undermining their operational independence, which they have fervently guarded for decades. At the same time, it exposes the world economy to a series of largely untried and untested monetary policy strategies.

Consequences: rising government debt and low interest rates

The net result is that world government debt has more than doubled in the last 12 years. It has risen from less than $33 trillion (57% of world GDP), prior to the global financial crisis in 2008, to more than $70 trillion (91% of world GDP) in 2020. This represents an average annual growth rate of over 6%, which is well in excess of the growth in global GDP over the same period. In addition, private sector debt (measured on a global basis) has jumped from $117.5 trillion during 2007 to $118.1 trillion in 2020.

A government’s ability to increase or sustain a high level of debt is highly dependent of three key factors, namely:

- the maturity profile of the debt

- the government’s ability to collect tax revenue, and

- the interest cost of the debt.

While the maturity profile of government has not altered substantially in recent years, the current recessionary conditions have clearly undermined government tax revenue collection. Fortunately, this has been significantly offset by a sustained reduction in global interest rates.

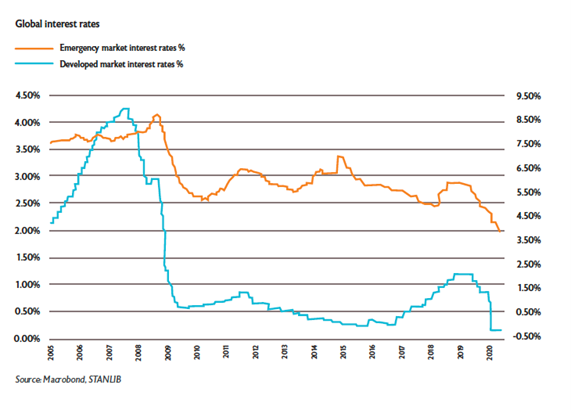

For example, policy interest rates in developed economies were recorded at a GDP weighted average of only 0.11% at the beginning of October 2020, which is a record low. At the same time, official interest rates in emerging markets have fallen to a GDP weighted average of a mere 3.9% – also a record low.

How does this play out?

The immediate and obvious uncertainty presented by this new normal of high government debt and record-low interest rates is the question of how most central banks will eventually unwind the current monetary stimulus – both in terms of the record-low interest rates, and also the unprecedented injection of liquidity.

Under these circumstances, even a small increase in interest rates could derail the global economy’s fragile recovery. Knowing the danger of a premature withdrawal of the highly accommodative monetary policy, few central banks will be willing to risk a severe recession in the pursuit of policy normalisation.

| In other words, no major central bank will want to be held responsible for crashing the financial markets because they started to reverse monetary policy without clear justification. |

Furthermore, even if the withdrawal of financial liquidity appeared fully justified, it is highly likely that it would still result in a significant sell-off in financial markets.

Moreover, with central banks now being the largest holders of many risky assets like government bonds, these banks will be mindful of how changes in monetary policy could damage the public sector’s own balance sheet, with dire consequences for stability in the broader economy.

Fortunately, in the short-term, global inflation remains extremely well-contained, with most countries currently more concerned about the risk of deflation rather than inflation. In fact, consumer inflation in the Euro-area has averaged less than 1% during the last eight years, while in the US, the average has been a mere 1.5% over the same period.

Furthermore, even if inflation does start to rise, the United States Federal Reserve has already signalled its willingness to tolerate price increases above their target of 2%, arguing that, since inflation has been below 2% for a considerable period, they should rather focus on the average rate of inflation and not merely a point target of 2%. Hence, without a persistent increase in inflation, many central banks may find it difficult to justify an exit from their supportive monetary policies.

Equally, should the existing fragile global economic recovery start to stall, it seems fair to assume that the major central banks will endeavour to introduce even more innovative policy tools, such as the purchase of highly risky assets, active control of the yield curve, and perhaps even greater use of negative interest rates.

Overall, the current global monetary policy of record-low interest rates and increased liquidity appears likely to persist for a considerable period, despite the obvious risks.

Under these circumstances, investors are having to fundamentally change how they take account of risk in constructing their portfolio, with a traditional low-risk portfolio providing a return well below the historical average.

In the meantime, any sustained emergence of consumer inflation around the world that might necessitate a tightening of monetary policy, will start to make central banks, governments and investors extremely nervous.

This article appears in the Q4 November 2020 edition of our StandPoint publication. Click here to download a copy of the full publication.