Investment opportunities in a changing world

Vaughan Henkel

Portfolio Manager, Absolute Returns Strategies

Thematic investing

Long-term thematic investments are those that benefit from structural changes to the world in which we live. These themes tend to be long-lived and provide significant performance advantages over time, if correctly identified.

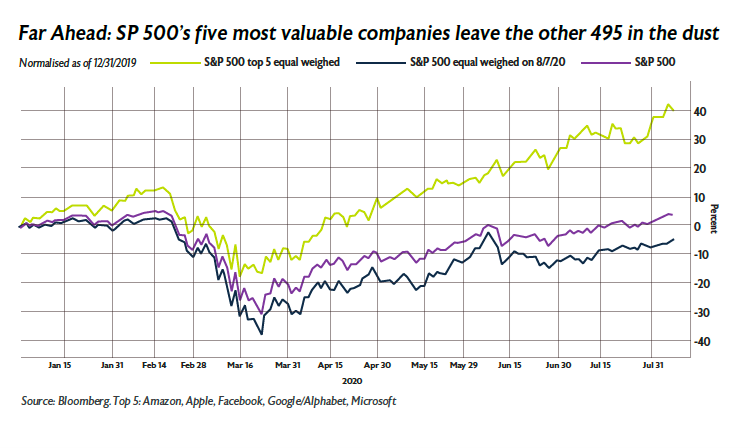

The latest and most recognisable structural change is the shift to digital socialising, shopping and entertainment, resulting in the recent FAANG (Facebook, Amazon, Apple, Netflix and Alphabet ,formerly Google, phenomena, where five technology stocks now constitute 37% of the S&P500 index. In 2020, these stocks have been the sole drivers of the index’s growth as the pandemic drives digital acceleration.

As these pandemic-led shifts continue to impact the longer-term sustainability of business, it is beneficial to recognise themes that are arising or those that are accelerating when constructing portfolios, thereby optimising exposure to areas of sustained growth.

What’s next?

Identifying a theme that will drive long-term growth, and finding ways to access companies or investments that will benefit from this theme, underpin the thematic investing concept. Environmentally-related themes have gained recognition over the last few years as the world aims to curb the adverse impact of various activities on our planet.

Clean energy

Clean energy is the creation and delivery of energy without harm to the environment. For the purpose of this analysis, we view it as non-oil types of energy. Once the focus of environmental activists only, championing cleaner ways to deliver energy or power has now become more mainstream for a number of reasons:

Governments

- The United Nations Paris Agreement, which was signed by countries worldwide, commits them to lowering carbon emissions, given the harmful impact on the environment.

- US President-elect Joe Biden, promises to direct US$2trn to clean energy, over the next four The US also plans to derive all electricity from carbon-free sources by 2035 (renewables were <10% of US Energy consumption in 2019).

- The EU climate plan targets at least a 55% reduction in carbon emissions by 2030, another key driver of clean energy. Indeed, the EU climate plan is to derive 40% of energy from renewables by 2030 (the share of production needs to rise from 32% to 65% by 2030 to achieve this).

- China derives only 3.2% of its electricity from wind and solar, but this is forecast to grow to 22% by 2040 at a CAGR of 6% – well above total electricity growth of 1.2% CAGR, from 2015 to 2040 (EIA stats).

Society

- The COVID-19 pandemic has renewed the focus on health and well-being, impressing on people the need to take physical precautions and measures to ensure not only a healthier life, home and working environment, but also the macro global environment.

- The current Gen-Zers, personified by child activist Greta Thunberg, are significantly more attuned to and focused on the sustainability of a healthy environment.

- The groundswell towards ESG as a ‘right to play’.

Business and investment

- Even Big Oil, as evidenced by BP’s recent plan to increase green energy by 50 Gw by 2030, has understood something clearly at last (Note green energy in the UK totals 50 Gw today).

- Furthermore, our analysis shows that this strategy (for selected ETFs) has kept pace with the S&P500 over the past eight years.

Clean energy: a sustainable theme?

Two primary indicators or drivers of the clean energy theme are capital expenditure (capex) and historical performance of clean energy investments relative to the tech phenomena stocks.

1. Energy capex

Over the last five years, the global clean energy capex has been tracking at approximately US$600bn per year, and largely flat over the period (IEA statistics). Global oil-related capex has, on the other hand, declined from US$875bn in 2014 to less than an estimated US$400bn in 2020 – a more than 50% drop. This demonstrates that the global shift in capital spent on energy has already been in play for the last five years, before the current focus on the environment (the E in ESG). The chart below (showing the latest year only) shows the increase in renewable power investment vs oil and gas.

The crisis is hastening the retirement of some older plants and facilities, but also dampening consumer spending on new and more efficient technologies,

Looking further out to 2050, we show how BP (in their new Energy outlook for 2020, September 2020) forecasts a rapid increase in clean energy capex, regardless of which type of carbon-reduction scenarios are accepted. The investment required in wind and solar alone (a clean energy subset), will be between US$500 and 750bn per year (in both carbon emission reduction scenarios of 70-95% by 2050). This is two to three times greater than the current level of investment.

2. Relative performance: Clean energy vs the S&P index

The performance of the Powershares Cleantech Portfolio (PZD), which tracks a global index of cleantech companies, has kept pace with the Standard & Poor’s index (SPX) over the last eight years (9.8% CAGR vs 9.9% for SPX), which is somewhat surprising given that SPX comprises many tech stocks. PZD is likely to outperform SPX into the future, with increasing attention to clean energy.

We also note how the PZD has greater drawdowns (bottom part of the chart) than the SPX. This is due to a smaller number of stocks, but it also highlights how a longer timeframe is required to offset the volatility.

Where does South Africa fit in?

South Africans are all too aware of the challenges we are experiencing with our main energy provider, Eskom, on a daily basis. The CEO of Eskom optimistically indicated to the market that we will only experience electricity challenges for another 18 months.

While coal provides the base-load for South Africa and will continue to do so for the foreseeable future, transitioning to more clean energy is critical for South Africa’s contribution to global carbon-emission reduction and to be in line with the Paris Agreement. The Integrated Resource Plan 2019, gazetted by the Department of Energy in October 2019, demonstrates this direction, and by 2030, 24.1% of SA’s energy contribution is expected to come from solar (PV) and wind.

As the world continues to drive change towards a cleaner environment, it’s a good time to invest in this thematic growth story. Investors are effectively collaborating with stakeholders across the world to drive a positive sustainable environmental impact, and will benefit from the resulting ‘clean’ financial returns.

This article appears in the Q4 November 2020 edition of our StandPoint publication. Click here to download a copy of the full publication.