A systematic approach to active management

Wehmeyer Ferreira

Chief Operating Officer STANLIB Index Investments

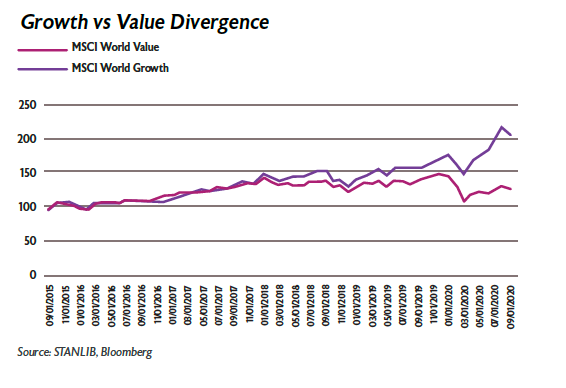

The two investment themes are well-covered in the media and financial literature. Various investment styles perform well over specific business cycles, and it is unlikely that a specific investment style would outperform others into perpetuity, although significant periods of outand under-performance can and have occurred. As such, what investors should be considering is how they can best position themselves to gain exposure to a specific or various investment style(s).

Another long-standing concurrent debate in the investment management field concerns the relative merits of passive versus active investing; or, put differently, the relative value of index tracking versus stock-picking.

STANLIB Index Investments is firmly in the camp that believes in the power of beta (broad market exposure) to deliver investment outcomes. However, we strategically sit in two camps – not something every asset manager is comfortable doing.

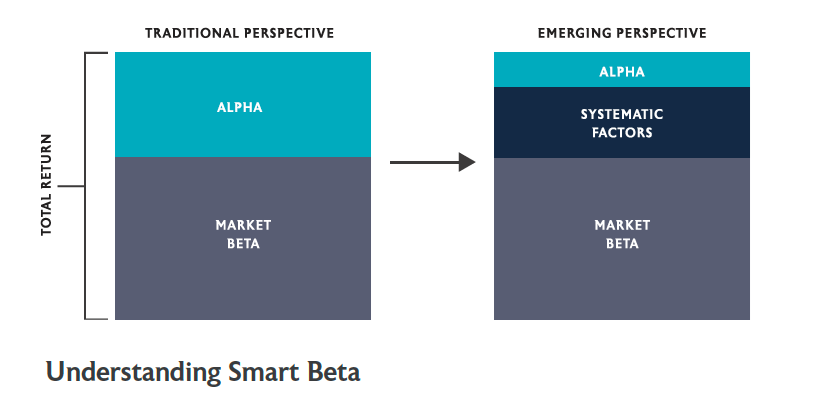

We also believe that outperformance of a market-cap-weighted index is possible through effective active systematic investing, which can be achieved by exposing investors to persistent drivers of return. Systematic investing follows a rules-based approach – taking the emotion out of investing when making investment decisions. Investment outcomes are based on these rules. Over the last decade, we have seen the steady rise of new types of investment funds, termed ‘Smart Beta’ and ‘Multi-Factor’. These funds may best be described as ‘systematic active’, due to the rules-based nature of investment management and the source of returns. The rise of Smart Beta is due to an evolution in investment thinking, where a large portion of what was previously considered to be alpha is now viewed as exposure to systematic styles or factors via Smart Beta funds (see Figure 1).

| ‘Smart Beta’, a specific systematic investing approach describes rules-based investment strategies that are based on specific market factors, for example, growth or value. |

A Smart Beta process passively tracks an index, but targets only the identified or chosen set of risk

factors expected to add value over time. This approach represents an ideal blend of passive and active

portfolio management styles, in a systematic quant-based approach. The main premise is that persistent

and systematic drivers of returns (the factors) exist in the market; therefore, combining these drivers in

an unemotional, systematic and rules-based way, leads to outperformance in the long term.

Active managers can be systematic managers

The aim of active management is simply to outperform a chosen benchmark through successful asset or security selection and portfolio construction. This is achievable when the active managers have an ‘edge’ over other investors (and the market), which allows them to identify superior investment opportunities and deliver optimal outcomes for investors. However, if the notion of active management creates the mental image of a fundamental active manager, you will need to adjust your thinking – active managers include systematic managers.

| The active manager’s ‘edge’ typically comes from better market information, better information processing systems, better investment processes, or better risk management. |

Systematic managers would argue that the four areas apply to them as well; but since a systematic process is followed, systematic managers can consume more market information, apply more processing power, and deploy an investment process and risk management system without any behavioural biases. As such, systematic managers are very much active managers.

The STANLIB Index Investment team has discussed in a previous STANDPOINT article, Tilting Towards Opportunities in the Midst of a Crisis, how different styles and factors perform in various market conditions.

This demonstrated the robustness of style/factor investing at the height of COVID-19, but it also applies through any business and/or economic cycle. If we look at the three STANLIB Smart Beta products, and their performance year-to-date versus broad market indices (see Figure 3), style leaders and laggards are clearly observed. But these results are not unique to this tumultuous year. Different individual investment factors outperform and underperform from year to year, as mentioned earlier.

Investing in Smart Beta

Single-factor Smart Beta funds are typically used by investors as:

1) a long-term investment to buy and hold through an entire business and economic cycle (which could be more than 10 years for full benefit); or

2) a product or building block investment to complement or complete an existing equity portfolio; or

3) a tool to take advantage of a specific outlook on the cycle or a factor.

However, investing in Smart Beta funds requires dynamic allocation and risk management by an investor to ensure an optimal outcome. Periods of volatility and underperformance will test the best investors and expose them to unavoidable and natural behavioural traits, often leading to adverse asset allocation decisions.

For this reason, when the STANLIB Index Investment team considers what our best equity view and approach is, we refer to the Multi-Factor approach. Multi-Factor funds offer investors simultaneous exposure to more than one investment factor (style). The investment process combines the benefits of Smart Beta, allocation to proven factors or style, and sound portfolio construction (where we combine factors in the most optimal manner).

Top-down or bottom-up factor allocation

Multi-Factor strategies can be implemented with two different approaches: top-down or bottom-up factor allocation.

Top-down Multi-Factor funds blend single-factor or Smart Beta, portfolios to create a diversified equity portfolio. Bottom-up Multi-Factor funds score individual shares on multiple factors, which translates into a multi-factor score per share. The stocks with the highest multi-factor scores are then included in the multi-factor portfolio. While these definitions oversimplify the full processes of both methods, in this article they serve to give a high level of understanding.

The STANLIB Index Investment team is of the firm belief that utilising a bottom-up approach delivers the most robust result. This approach creates a targeted portfolio with higher factor exposure or factor purity, which should deliver superior long-term risk-adjusted returns. The image below shows our approach to bottom-up factor allocation.

Rules-based, data-driven, and multi-style focused investment approaches offer investors and asset allocators a return outcome that is not influenced by behavioural biases. Smart Beta funds based on individual factor allocation are ideal for existing portfolio style enhancements or existing portfolio risk mitigation. Concurrently, we believe that the multi-factor approach will achieve consistent long-term results by allocating to multiple and prevalent investment styles.

This article appears in the Q4 November 2020 edition of our StandPoint publication. Click here to download a copy of the full publication.